From the Desk of Our CIO

The Fertilizer Front: How the Iran War Is Repricing the Commodity Complex

Executive Summary

- Almost a month into the Iran conflict, de-escalations are underway, but none constitute a credible off-ramp.

- Iran’s leverage is real and Tehran may not yet believe it has extracted sufficient deterrent value to stand down.

- A ground force operation targeting Kharg Island, which handles up to 90% of Iran’s oil exports, would risk an acute retaliatory response, and is a significant escalation risk.

- The Houthis entering the conflict as the second-front threat is not symmetric. Asian cargoes, the bulk of Gulf crude demand, must transit Bab el-Mandab with no practical alternative. Should the Houthis activate, Saudi Arabia’s bypass loses its value for the buyers who need it most.

- This conflict is not just an oil story. The Hormuz closure has shut in Gulf natural gas production, the feedstock for ammonia and urea. With no strategic fertilizer reserves and no pipeline bypass for ammonia, urea prices are skyrocketing, arriving precisely at the Northern Hemisphere spring planting window.

- The fertilizer shock has hit the grain complex asymmetrically and may not yet be fully priced. Corn and canola face the greatest input cost exposure, while hard red winter wheat (HRW) is more affected than soft red winter wheat (SRW), while soybeans are largely insulated. The crude oil rally is simultaneously transmitting into agricultural markets through the biofuel channel, repricing soybean oil, palm oil, and sugar in ways that extend well beyond the energy complex.

- Viewpoint Diversified Commodities’ risk parity framework captures this dispersion. The most liquid commodities are not always the most affected, and geographical and supply-source diversification within a sector matters most precisely when markets are under stress.

The Fertilizer Front: How the Iran War Is Repricing the Commodity Complex

Since my last note two weeks ago, the strategic calculus for both sides has not fundamentally changed. While there have been meaningful, if incomplete, de-escalations worth tracking, these developments have not produced a credible resolution path.

Iran continues to export approximately 1.5 million barrels per day through the Strait of Hormuz, earning record oil revenues in the process. Iran’s Foreign Minister announced that vessels from China, Russia, India, Iraq, and Pakistan would be permitted to transit the Strait, a signal that Tehran is actively managing its leverage rather than simply closing the tap. The U.S. has issued 30-day sanctions waivers on Iranian oil stranded at sea, covering roughly 140 million barrels, and earlier extended a comparable waiver on Russian crude, both moves aimed at loosening the tightening noose on energy markets. Saudi Arabia has activated its East-West pipeline, transiting through Yanbu to the Red Sea, while the UAE has ramped Fujairah exports to approximately 1.9 million barrels per day, running 57% above last year’s average flow. Together the Saudi and UAE bypass options provide just under 6 million barrels per day of flow, meaningful but still insufficient relative to normal Strait volumes. The U.S. has also extended its pause on striking Iranian energy infrastructure, preserving a negotiating surface. And while Iran publicly denies that formal talks are underway, the fact that Tehran is set to formally respond to the U.S. 15-point peace proposal, which demands nuclear rollback, ballistic missile limits, cessation of proxy support, and the reopening of Hormuz, suggests back channel engagement through mediators is almost certainly active.

Perhaps the most telling signal is the scheduling of a Trump-Xi summit in Beijing for May 14th and 15th, rescheduled from late March after the war began. The White House originally estimated a four-to-six-week window for conflict resolution from the February 28th start date. Scheduling a high-stakes bilateral summit with China for mid-May reflects, at minimum, a working assumption in Washington that this conflict will not still be in an acute phase by then.

And yet, taken together, these developments do not add up to a clear off-ramp. De-escalation at the margins is not the same as resolution. The U.S. has strong incentives to bring this to a close as gas prices are rising, consumer affordability concerns are compounding, financial conditions are starting to tighten, and the likelihood of Democrats flipping both chambers of Congress is increasing. But Iran must be a willing party to any negotiation, and Tehran’s calculation may be that it has not yet extracted sufficient pain from the global economy to guarantee that a similar confrontation does not arise again in the near future. That being said, the regime’s leverage is real and time limited. Hormuz cannot be closed indefinitely without eliciting a coordinated global response to reopen the Strait once global inventories are drawn down and shortages begin to occur. However, Iran may not yet feel it has banked enough of a deterrent dividend to declare the confrontation a strategic victory and stand down.

The most significant near-term escalation risk on the U.S. side is the reported preparation of ground force options potentially targeting Kharg Island, the strategic Persian Gulf hub that handles up to 90% of Iran’s oil exports. The Pentagon has reportedly positioned elements of the 82nd Airborne Division and Marine Expeditionary Units in the region, and while most analysts interpret this as coercive leverage to strengthen Washington’s negotiating hand rather than a concrete invasion plan, Iran has responded by fortifying the island with anti-personnel and anti-armor mines along its shoreline. A miscalculated move in either direction would materially change the trajectory of the conflict. Any boots on the ground would likely result in a further escalatory response from Iran, along with an increased risk of attacks in the Red Sea.

Yemen’s Houthis, who suspended attacks on shipping following the Gaza ceasefire in October 2025, have publicly declared readiness to resume operations in solidarity with Tehran, and there were reports on Friday that they will now officially enter the conflict in support of Iran. Follow-through from the Houthis on these reports would certainly change the calculus of the conflict. From Yanbu, European-bound tankers can head north through the Red Sea toward Suez, moving away from Houthi-controlled territory, and while there is still some risk from long-range Houthi missiles, it remains manageable. Asian cargoes, which represent the bulk of Gulf crude demand, have no equivalent escape. Any ship heading south from Yanbu toward the Indian Ocean must pass through the Bab el-Mandab strait, directly through Houthi-threatened waters, and there is no practical alternative routing. Even a Cape of Good Hope diversion requires transiting Bab el-Mandab first. Iran has already tested the vulnerability of the bypass infrastructure directly, striking Yanbu’s Samref refinery with a drone and firing a missile at the port itself, which was intercepted. Should the Houthis credibly activate, Saudi Arabia’s pipeline bypass may become compromised without safe shipping passage. Global energy markets would then face the simultaneous effective closure of both the Strait of Hormuz and the Red Sea, a dual chokepoint scenario with no historical precedent for rerouting at that scale.

Even without an escalation, the clock is ticking before oil inventories are drawn down to a point where closures start to create genuine demand destruction. While much has already been written about the disruption to oil markets, the market has been slower to price the secondary transmission risk. As I discussed in my last note, when Iran effectively shuttered the Strait, it also shut in a significant portion of Gulf natural gas production. Natural gas is the primary feedstock for ammonia, the building block of every major nitrogen fertilizer including urea. Approximately 30% of globally traded urea originates from Hormuz-constrained producers, and QatarEnergy has halted ammonia and urea production. Unlike crude oil, there are no strategic fertilizer reserves, and no pipeline bypass exists for ammonia.

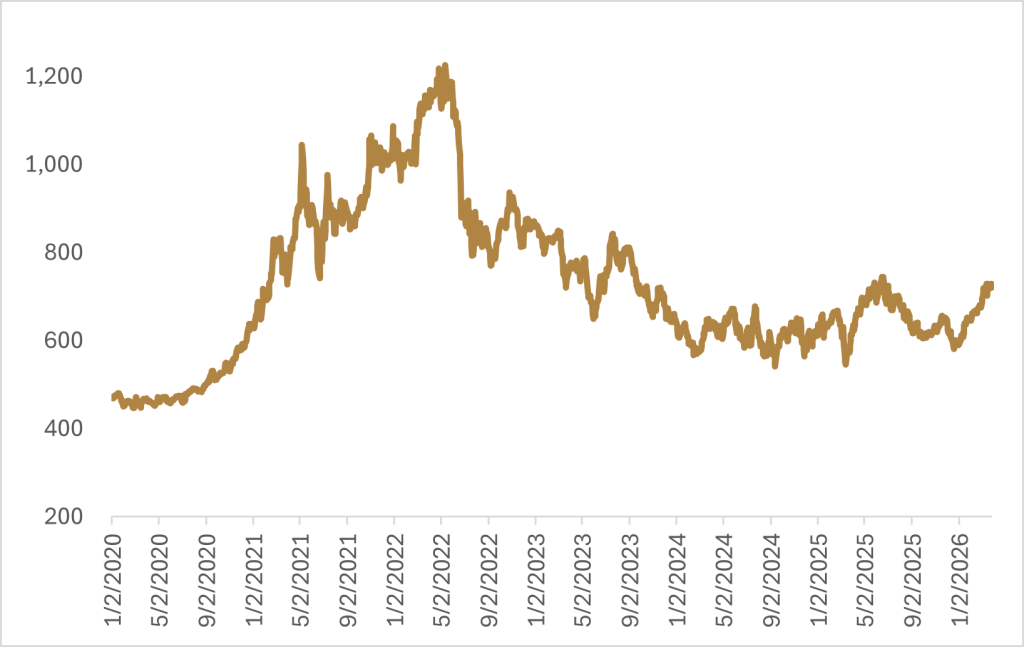

The timing is punishing as spring is when North American farmers apply the bulk of their nitrogen. Gulf vessels require roughly 30 days to reach U.S. ports, plus three to four weeks to farm delivery. Cargo not already on the sea risks missing the planting window entirely. The result is that urea at the New Orleans import hub, the benchmark price for U.S. farmers, has jumped from $462 per metric ton on February 27th to $630 per metric ton on Friday. Farmers who have not contracted enough fertilizer for the planting season face three choices. They can pay the higher price, reduce application rates and accept lower yields, or shift to less nitrogen intensive crops. All three have consequences for grain prices, and the market is beginning to reflect them.

The fertilizer shock does not hit the grain complex uniformly, with nitrogen intensity varying materially by crop. Corn is the most nitrogen hungry major crop in North America, requiring 150 to 200 lbs per acre, and is the single largest consumer of synthetic nitrogen on the continent. Its economics are directly and immediately exposed to urea price spikes, with front-month futures up 3% month-to-date and the futures curve steepening with upward price pressure on fall and winter contracts.

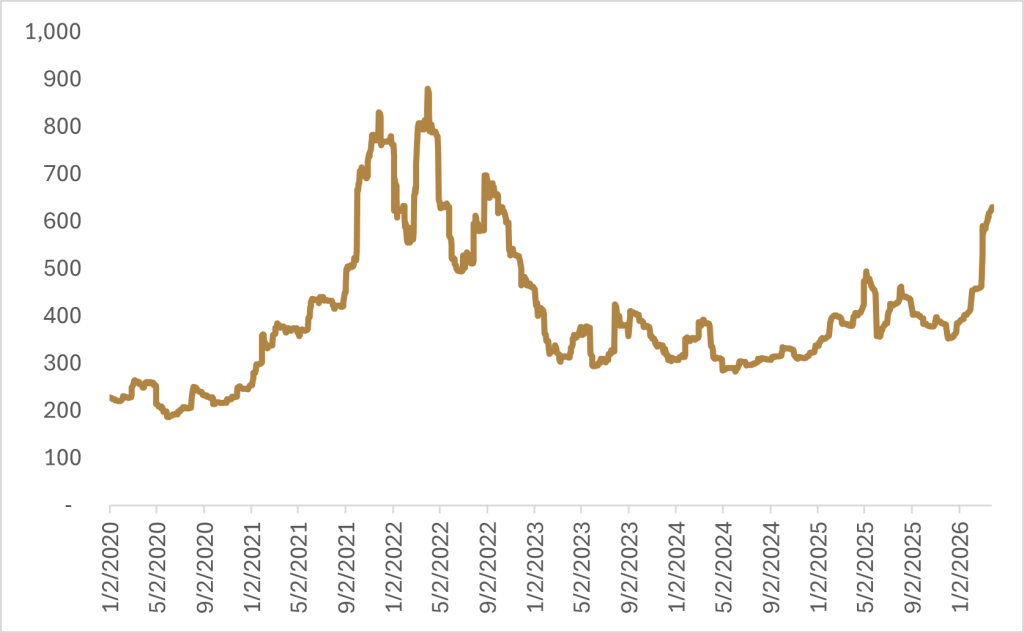

Canola is similarly intensive and is actually more nitrogen demanding per bushel of yield than wheat. It is also a significant biofuel feedstock in Europe and Canada, giving its dual exposure to both the input cost channel and the crude oil rally. Front-month canola futures are also on the rise, up 5% month-to-date.

On the wheat side, hard red winter wheat (HRW) must meet protein content thresholds, typically 12 to 14%, to satisfy bread flour millers. Producers often over-apply nitrogen to reach those thresholds, making HRW structurally more nitrogen dependent than its soft wheat (SRW) counterpart, which deliberately targets lower protein and therefore lower nitrogen applications. Compounding the input cost story, a persistent La Niña-driven drought has gripped Kansas, Oklahoma, and Texas since last autumn. Kansas winter wheat ratings have dropped 22% in the past month alone, with the Brugler500 index falling to a poor reading of 339. The combination of drought and HRW’s heavier nitrogen burden has opened a nearly 7% gap between HRW and SRW this month, a compelling illustration of why commodity diversification matters even within the same sector. While investors may think all wheat is the same, during stress events supply chain dislocations can drive meaningful divergence between contracts that appear fungible under normal conditions.

A planting season cost shock of this magnitude, arriving in a year when corn and canola margins are already under pressure, will likely shift some acreage toward soybeans. We saw exactly that pattern following the 2022 fertilizer shock after Russia’s invasion of Ukraine. The resulting acreage shifts tighten corn and canola supply further, compounding the direct price impact of higher input costs.

Within the grain complex, soybeans are relatively insulated. They fix atmospheric nitrogen through root bacteria and have minimal synthetic nitrogen requirements, making the fertilizer shock largely irrelevant to their input economics. Soybean oil, however, has spiked for a different reason entirely, as the surge in crude oil has driven excess demand for biodiesel feedstock across the vegetable oil complex. When energy prices spike, vegetable oils that can substitute for petroleum as biodiesel and renewable diesel feedstock reprice quickly. Soybean oil, the primary feedstock for North American renewable diesel, has been the clearest expression of this, jumping 9% month-to-date as blenders compete for available supply and crush margins widen.

The same dynamic is visible in palm oil, the dominant biofuel feedstock in Southeast Asia. Indonesia fast-tracked its B50 blending mandate when crude crossed $110 per barrel, effectively pulling an estimated 3 million additional tonnes of palm oil off international export markets and triggering palm oil’s largest single-day move since 2022. Vegetable oils globally are expressing the same transmission from crude markets to biofuel demand, with soybean oil being the North American expression of that trade.

It extends to sugar as well. Brazil is the world’s largest sugarcane producer, and its mills face a perpetual allocation decision between processing cane into raw sugar for export or diverting it into ethanol for the domestic fuel market. When crude oil is at $100 or above, ethanol economics become significantly more attractive and mills shift their mix accordingly, reducing raw sugar output, tightening global supply, and lifting sugar prices. Raw sugar futures jumped more than 13% as the crude surge rippled through that calculation. The broader sugar market still carries a structural surplus, so this rally is energy driven rather than a fundamental supply story, but the mechanism is real. It illustrates how a conflict centered on an oil chokepoint can reach into the agricultural commodity complex through multiple and sometimes unexpected channels.

The fertilizer shock is a lagged transmission mechanism. Planting season disruptions in spring 2026 will not fully appear in grain supply data until the summer crop reports and fall harvest. The market is beginning to price this, but grain futures curves steepening does not yet fully reflect a scenario where urea prices remain elevated and acreage shifts materially toward soybeans.

Viewpoint Diversified Commodities’ risk parity framework sizes positions to equalize risk contribution across the complex rather than concentrating in the most liquid names. The result is meaningful weights in HRW, canola, and soybean oil alongside the more familiar grains, which is important for investors looking for a well-diversified basket that can harvest unique inflation risk premiums across various supply shock transmission channels.

The most liquid commodities are not always the most affected. While commodities within the same sector may appear fungible during normal market conditions, during stress events they can diverge in ways that matter significantly for portfolio outcomes. Geographical diversification and diversification across supply sources for similar commodities both matter, and this month has been a clear demonstration of why.

The Iran war began as an energy story, but it is quickly becoming a food story. The Strait of Hormuz closure has interrupted not just oil flows but the nitrogen supply chain that underpins North American grain production, and it has done so at the worst possible moment in the agricultural calendar. The off-ramp remains available but is not widening. Extension of the conflict through April materially increases the probability that current supply disruptions translate into not only energy shortages, but increasingly food price inflation, a transmission channel not yet fully reflected in commodity prices.

In a multipolar world where geopolitical shocks are becoming structural rather than episodic, proper commodity exposure is not just tactical positioning, it is imperative for robust portfolio infrastructure.

Scott Smith

Chief Investment Officer

ABOUT THE AUTHOR

DISCLAIMER:

This blog and its contents are for informational purposes only. Information relating to investment approaches or individual investments should not be construed as advice or endorsement. Any views expressed in this blog were prepared based upon the information available at the time and are subject to change. All information is subject to possible correction. In no event shall Viewpoint Investment Partners Corporation be liable for any damages arising out of, or in any way connected with, the use or inability to use this blog appropriately.