From the Desk of Our CIO

Iran Week Two: The Off-Ramp Is Narrowing and the Risks Are Broadening

Executive Summary

- As we enter the second week of the conflict, there has been no meaningful de-escalation, with attacks reported on Iranian oil infrastructure and desalination facilities in both Iran and Bahrain.

- Iran has named Mojtaba Khamenei as the new Supreme Leader, reinforcing regime continuity and confirming our view this isn’t a Venezuela-style situation with a cooperative successor waiting in the wings.

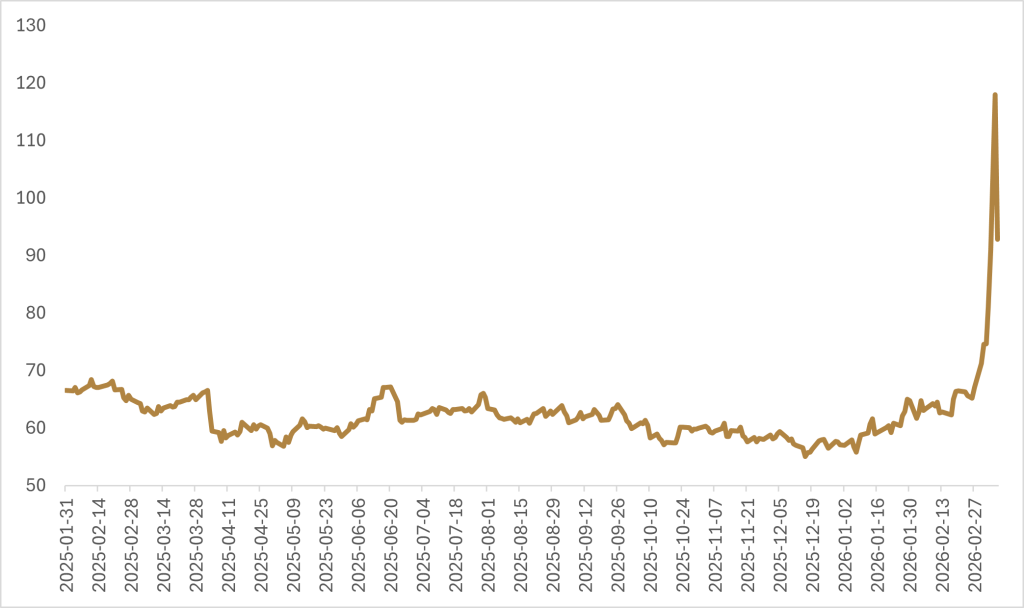

- JP Morgan estimates crude shut-ins have now reached 3.5–4.0 million barrels per day (bpd), and crude flows through the Strait of Hormuz (SoH) have declined by ~10 million bpd, larger than any single disruption during the Russia-Ukraine conflict – this caused WTI to briefly spiked toward $120/barrel Sunday night.

- The G7 is coordinating a potential SPR release of 300–400 million barrels. The headline is large, but logistical constraints mean the short-term replacement of lost barrels will be partial at best.

- Europe and Asia face materially greater exposure to this shock than the U.S., which is showing up in relative equity performance and a strengthening U.S. dollar. The ECB now faces the uncomfortable prospect of hiking into a supply shock.

- The conflict is no longer just an energy story. Around one-third of urea fertilizer originates in the Middle East, and much of those exports transit through the SoH, and there is no meaningful alternative route or strategic reserve to buffer a prolonged disruption. Food price inflation is now a second-order risk that markets are beginning to price.

- The most likely path remains regime calibration and a negotiated off-ramp with new Iranian leadership, but the window for a contained outcome is narrowing. If there is no resolution by the end of April, the probability of a global recession begins to rise materially.

- Commodities continue to perform their role as a geopolitical hedge, and their strategic importance in diversified portfolios has only been reinforced by the events of the past two weeks.

Iran Week Two: The Off-Ramp Is Narrowing and the Risks Are Broadening

Last week I argued that the Iran operation was more analogous to regime calibration than regime change, and that the lack of a credible, Western-aligned successor made a clean transition unlikely. The events of the past several days have done little to change that framing, and in some respects have reinforced it.

Iran has named Mojtaba Khamenei, son of Ayatollah Ali Khamenei, as the new Supreme Leader. Whatever one might have hoped from the succession process, it does not appear that is has been achieved. Mojtaba Khamenei represents institutional continuity, not a systemic break, dashing hopes for a Venezuelan Delcy Rodríguez equivalent. The elevation of the younger Khamenei does not preclude a negotiated off-ramp, but it does mean any deal will need to be made with people who are structurally committed to the survival of the existing regime, and likely on terms that reflect that reality.

The physical disruption to energy markets has continued to worsen. Israeli attacks on Iranian oil infrastructure and Iraqi oilfield shut-ins have exacerbated the already tight market environment. JP Morgan estimates that crude oil shut-ins have now reached 3.5 to 4.0 million bpd and crude oil flows through SoH are down ~10 million bpd, a number that, for context, exceeds the peak disruption attributable to the Russia-Ukraine conflict. WTI briefly made a run for $120 per barrel Sunday night before pulling back. Brent crude, Rotterdam coal, Dutch natural gas, and UK natural gas, remain sharply elevated, and refined product markets are tightening as both crude availability and refinery economics deteriorate.

The Sunday night spike in WTI prompted a coordinated G7 response, with discussions underway around a combined strategic petroleum reserve (SPR) release in the range of 300 to 400 million barrels. The headline number is the largest ever discussed for a coordinated release, and it will be helpful in arresting near-term panic. But the logistical reality is more sobering than the announcement.

During the last major SPR release in 2022, the U.S. released approximately one million bpd, slower than expected, reportedly due to structural constraints at storage facilities, while the IEA collectively contributed around two million bpd from member nations. Translating a 300-to-400-million-barrel headline commitment into actual market relief is therefore a process that takes time, involves infrastructure constraints, and is unlikely to fully replace ~10 million bpd of lost flow through the SoH in the near term. It should help to moderate the price spike and anchor some of the worst-case tail in energy markets, but it does not solve the problem, it just buys time while a diplomatic solution is sought.

It is also worth noting that the motivation for a coordinated SPR release is genuinely multilateral, not just a U.S.-driven response. Europe and Asia are far more exposed to imported energy price shocks than the United States, which has greater domestic production flexibility. This asymmetry is showing up clearly in financial markets with European and Asian equities selling off materially harder than U.S. equities, while the U.S. dollar has strengthened as a safe haven, adding a further terms-of-trade headwind for energy-importing economies already absorbing higher crude and LNG costs.

For Europe, this is a genuinely difficult macro scenario. The European Central Bank (ECB) now faces the prospect of having to hike interest rates later this year to head off an energy-driven inflation resurgence, at the same moment that the European economy is absorbing higher input costs and a weakening euro. This is the worst version of the central banker’s dilemma, hiking into a supply shock that is simultaneously raising prices and depressing growth. It is the same dynamic that made global central banks so reluctant to tighten in the early stages of post-COVID inflation and again following Russia’s invasion of Ukraine. The ECB will be wary of repeating that mistake, but the political and economic cost of preemptive tightening into a potential recession is not trivial.

The market conversation has been dominated by crude oil and LNG, but there is a second-order disruption building that deserves more attention: fertilizer. Roughly a quarter to a third of globally traded fertilizer transits the SoH, approximately 15 million tonnes of urea and ammonia annually, along with 22% of global phosphates, and nearly half of globally traded sulfur, a critical upstream input for phosphate production. QatarEnergy has already halted urea and ammonia output at Ras Laffan, and Iranian producers have suspended operations as well.

Unlike crude oil, there are no pipeline bypass options for fertilizer. Oman’s deep-water ports — Salalah, Duqm, and Sohar — sit outside the SoH on the Arabian Sea and have emerged as the region’s most viable transshipment alternative, and some producers are trucking volumes overland to reach them. There is also modest Red Sea capacity, with Morocco remaining a meaningful phosphate exporter and Saudi Arabia rerouting some volumes via Yanbu. But these are partial offsets. The sheer volume that normally transits the Strait cannot be replicated through these channels in any near-term timeframe, and the overland logistics add cost and delay that erode the economics of every workaround.

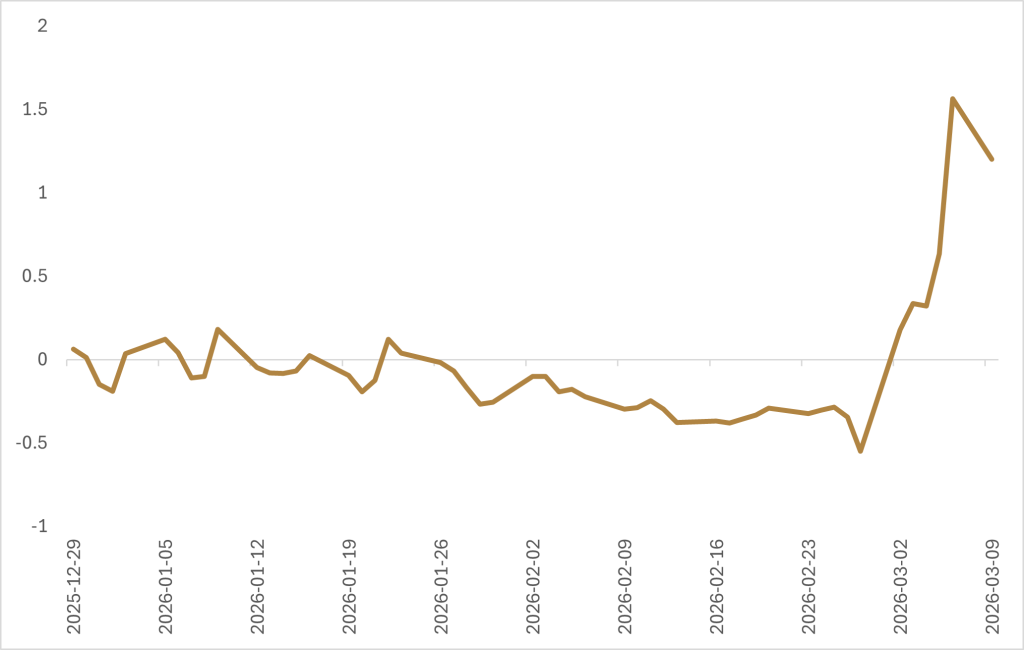

Timing makes this worse. A vessel loading in the Persian Gulf today takes roughly 30 days to reach U.S. shores, plus another three to four weeks to reach the farm. Any cargo not already in transit risks missing the Northern Hemisphere spring planting window. Unlike energy, there is no strategic reserve for nitrogen fertilizer and no SPR equivalent to bridge the gap. If the SoH remains closed through April, today’s supply disruption becomes next quarter’s food price problem, and that lagged transmission is not yet fully reflected in markets, though grain futures curves are starting to steepen.

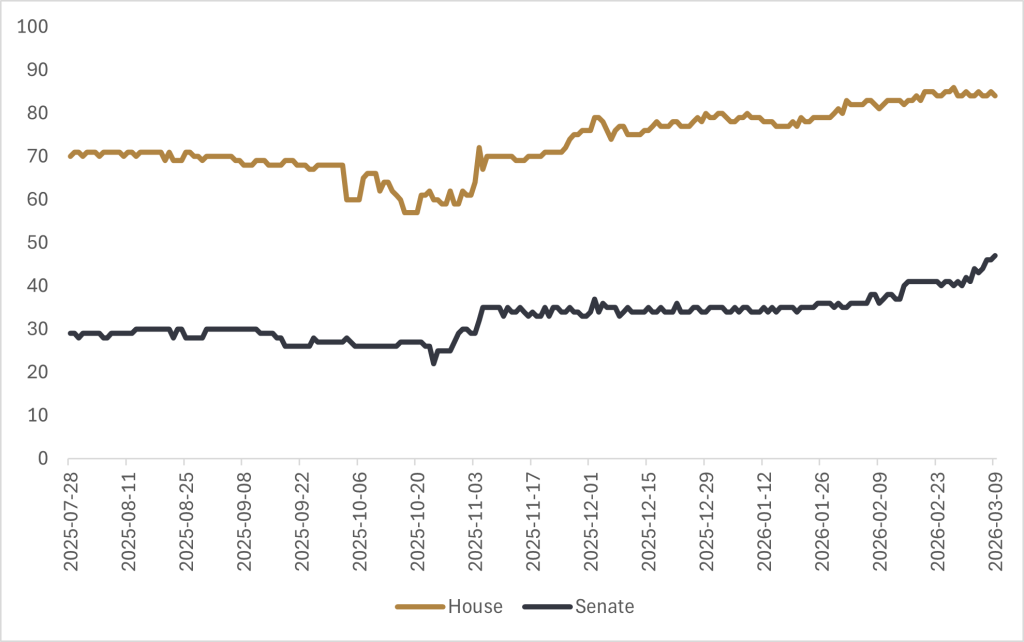

We talked last week about the U.S. administration’s midterm constraints, and those remain relevant. But over the past several days it has become more apparent there is an increasing possibility that the administration is already looking past the midterms as a potentially foregone conclusion. The probability of losing control of at least one chamber of Congress has moved meaningfully higher, and the Senate, which historically was the chamber far less likely to flip, is now showing genuine vulnerability. If the administration has mentally shifted toward legacy framing rather than midterm optimization, the political calculus and the time frame for an off-ramp changes somewhat.

That said, even legacy considerations have hard constraints. Sustained oil prices above $100 per barrel that eventually tip the global economy into recession are not a legacy any administration wants to own. Oil prices in the $120 to $150 range, if maintained for more than a few weeks, begin to generate demand destruction, corporate margin compression, and consumer confidence deterioration that feeds back into financial markets in ways that are increasingly difficult to contain. The administration has shown discomfort with Israel’s targeting of Iranian oil infrastructure, and that tension could serve as a constructive wedge. If the U.S. can position itself as having sought to limit civilian and economic damage while pursuing legitimate security objectives, it creates a diplomatic surface on which to begin building an off-ramp with new Iranian leadership.

My base case remains that the most likely path is regime calibration and a negotiated arrangement with Mojtaba Khamenei’s leadership structure, potentially centered on limits to enrichment activity and ballistic missile programs, in exchange for a cessation of active hostilities. It will be messy, probably won’t resolve the underlying deterrence problem as I argued last week, and it will likely be revisited in some form within a few years. But it probably represents the least-bad outcome available to all parties in the near term.

The key variable is timing. If there is a credible off-ramp by March, the economic damage should remain contained. A sharp but temporary spike in inflation expectations, some tightening of financial conditions, and a Q1/Q2 GDP drag that is recoverable. If the conflict extends into April without a resolution, the calculus shifts. Fertilizer disruptions begin to translate into planting-season impacts. Refinery margins tighten further. Consumer confidence, already under pressure from pre-existing affordability stress, takes another leg lower. At that point we begin to have a serious conversation about whether the global economy is on a path toward recession.

Through all of this, commodities have been doing exactly what they are supposed to do in a diversified investment portfolio. The geopolitical risk premium embedded in energy markets has repriced sharply, and the diversification beyond WTI and Brent into global LNG benchmarks and Rotterdam coal has added meaningful breadth to this hedge, exactly as we argued it should in a scenario where the Strait of Hormuz is the chokepoint for many different commodities.

The fertilizer and food price channel reinforce a point I have been making for several years. Commodity exposure in a diversified portfolio is not just a hedge against demand-driven inflation or energy price cycles. It is a hedge against physical supply chain fragility in a world where decades of underinvestment, geographic concentration of production, and geopolitical fragmentation are combining to make commodity markets more prone to nonlinear shocks. This week’s example, where a single chokepoint is simultaneously disrupting crude, LNG, ammonia, urea, sulfur, and phosphate flows, is a vivid illustration of why breadth of commodity exposure matters and how energy disruptions can spill over to grains and foodstuffs.

The near-term environment continues to favour holding existing commodity exposure and remaining cautious on long-duration assets, particularly in Europe where the ECB rate path has become more uncertain. For equities, the relative performance gap between U.S. and international markets is likely to persist until there is more clarity on the conflict’s duration. U.S. equities are not immune, earnings revisions will follow if energy costs remain elevated, but they are better insulated from the immediate transmission channel than Europe or Japan in the short-term. Where this calculus could flip is if we tip over into a global recession, and consumer stresses start to land ashore in the U.S. where the labour market is already weakening due to AI disruption. The vulnerability of software related private credit could create a larger delayed left-tail for private credit and public equities in the U.S. in this scenario.

The bottom line is that we are in a window where the off-ramp remains available, but it is narrowing. The most likely outcome is still a negotiated resolution, but the cost of delay is rising faster than most market participants appear to be pricing. In a multipolar world, where conflict is more frequent even if less structurally decisive, having the right commodity exposure is not a tactical trade, it is a structural feature of a resilient portfolio.

Happy investing!

Scott Smith

Chief Investment Officer

ABOUT THE AUTHOR

DISCLAIMER:

This blog and its contents are for informational purposes only. Information relating to investment approaches or individual investments should not be construed as advice or endorsement. Any views expressed in this blog were prepared based upon the information available at the time and are subject to change. All information is subject to possible correction. In no event shall Viewpoint Investment Partners Corporation be liable for any damages arising out of, or in any way connected with, the use or inability to use this blog appropriately.