From the Desk of Our CIO

The Bitter Truth: Why Your Morning Coffee Costs More & What’s Brewing for the Future

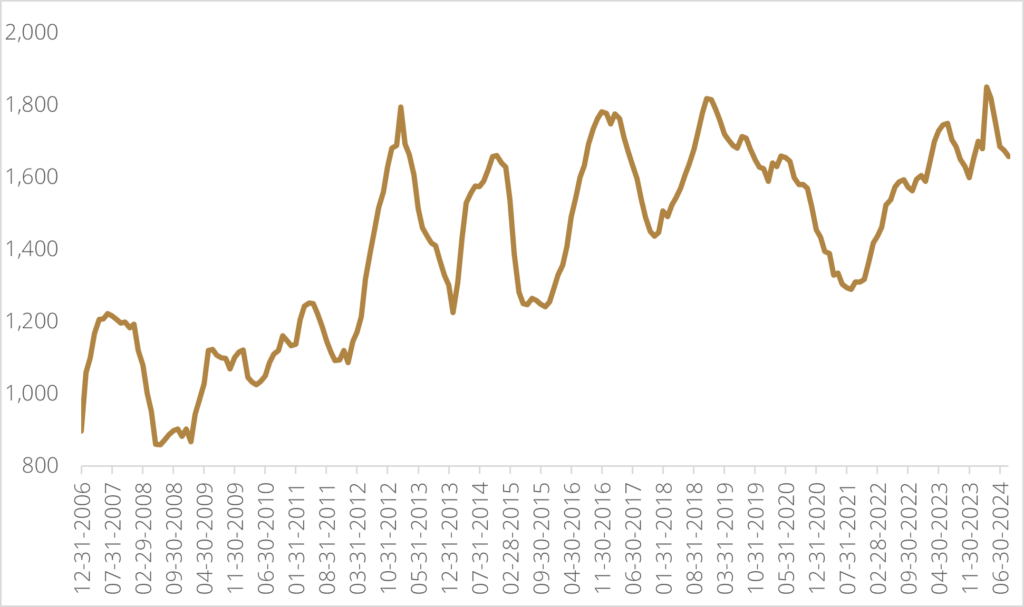

A key pillar of both U.S. political parties’ economic platforms is delivering a plan aimed at reducing consumer prices, which has been a major issue on both a local and global scale. In a recent note, we showed that the pace of rising food prices has been slowing, yet individuals are still unhappy with the cost of heading to the grocery store. An area where prices have not showed any signs of slowing down has been your morning java, with both higher-end Arabica and more budget-friendly Robusta beans increasing in price this year due to supply disruptions and increased demand from China. With Arabica and Robusta coffee futures increasing by ~35% and ~80% respectively year to date, many roasters were forced to raise prices back in July, passing along some of the increasing raw material costs to consumers.

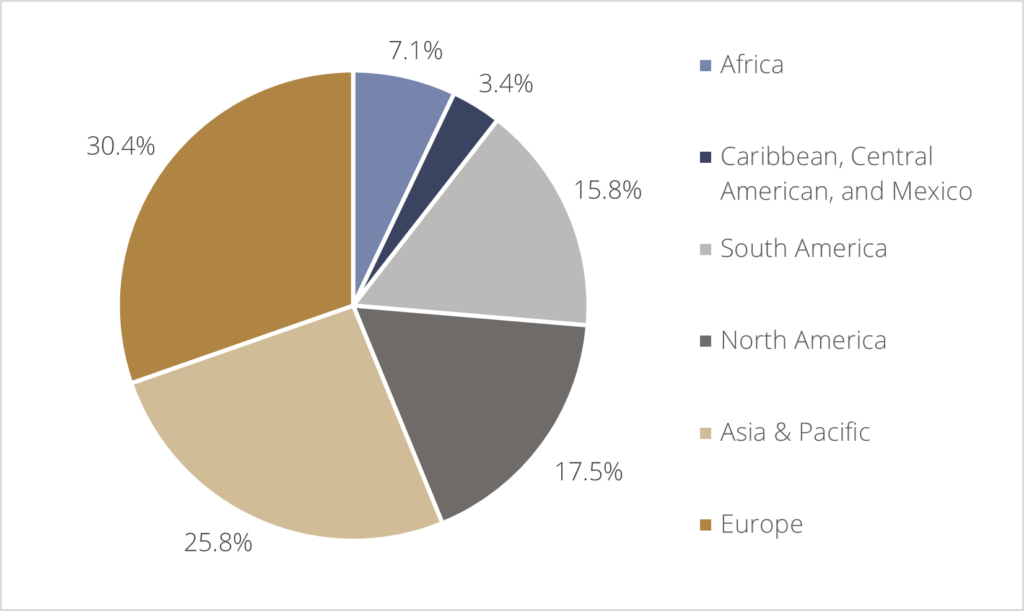

We wrote a note back in April about how a lack of origin diversification for soft commodities such as coffee, as well as cocoa and orange juice, was a risk for increased fragility in the supply chain with weather events having an outsized impact on production. Brazil and Vietnam account for almost 60% of global coffee production, with small origin producers from over 40 other countries making up the rest of global supply. Back in April, the spike in Arabica prices was due to fears that heavy rainfall in a Brazilian region that accounts for 30% of the country’s Arabica production would damage the crop. However, worries have now turned to drought conditions that could affect the flowering period for next year’s crop. This year’s crop was already disappointing for yields, as excessive heat and drought harmed development during last year’s flowering period at the end of 2023, producing a harvest this year with much smaller than usual beans. Vietnam, the world’s top exporter of Robusta beans, has also been dealing with drought conditions for most of this year and was hit with a typhoon just last week that might put further stress on the country’s Robusta fields.

With Brazil and Vietnam both dealing with challenging weather patterns, the smaller origin coffee beans from places like Ethiopia, Uganda, and Indonesia will become more integral to global coffee supplies, although it’s unlikely this will help to materially lower prices in the short term. Smaller producers lack the production infrastructure and economies of scale to add meaningful production like Brazil and Vietnam at similar prices, with many of the smaller origin countries still relying on family farms that harvest by hand. Higher prices and consumers willing to pay more for small origin coffee will help direct capital into better production infrastructure, but much like the cocoa market, this supply chain diversification won’t happen overnight.

Adding fuel to the fire is the fact that the E.U.’s Deforestation Regulation (EUDR) is coming into effect at the end of the year. EUDR will require global commodity traders to prove that the imported commodity did not contribute to deforestation at any point during the supply chain lifecycle. Traders have been racing to secure physical supplies from the current Robusta crop, as the next crop to be harvested in October likely won’t land in Europe until the new year due to processing and shipping times, at which time the crop will have to be EUDR-compliant. Given that Europe is the largest coffee consuming region in the world—consuming 53.7M bags of coffee in 2023—traders and roasters don’t want to risk further supply disruptions in early 2025 if smaller origin exporting countries don’t have the proper EUDR programs in place. While these European regulations will increase costs for the small origin countries, and potentially upend supply chain diversification, this could provide an opportunity for Chinese demand to secure higher-end small origin coffee that needs to find consumption demand outside of Europe.

The upcoming European deforestation regulations may have pulled forward some bean demand, as we’ve seen inventories for both Arabica and Robusta increase since Q1 of this year. However, stock levels are still at relatively low levels from a historical perspective.

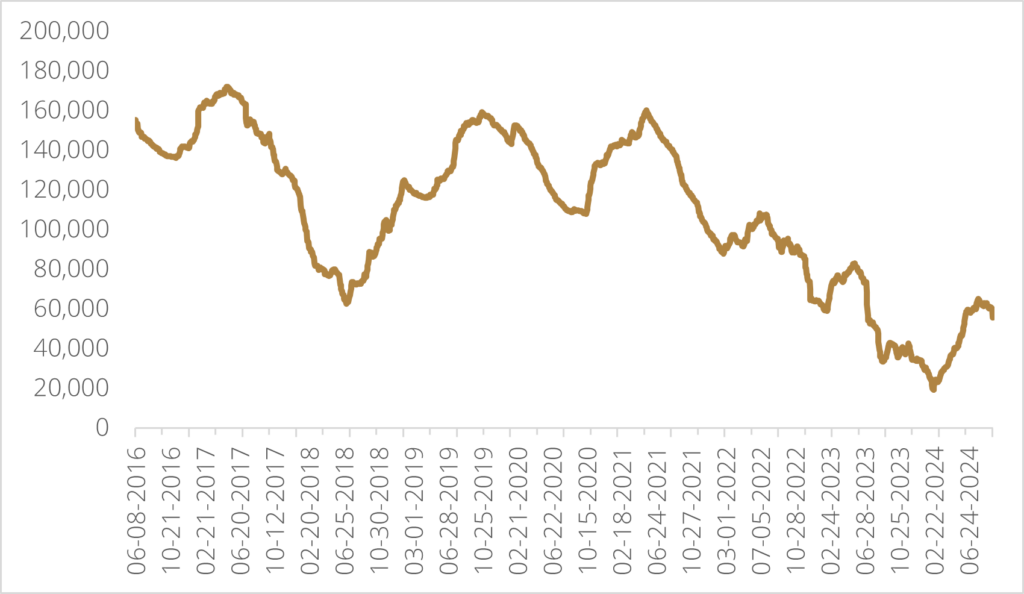

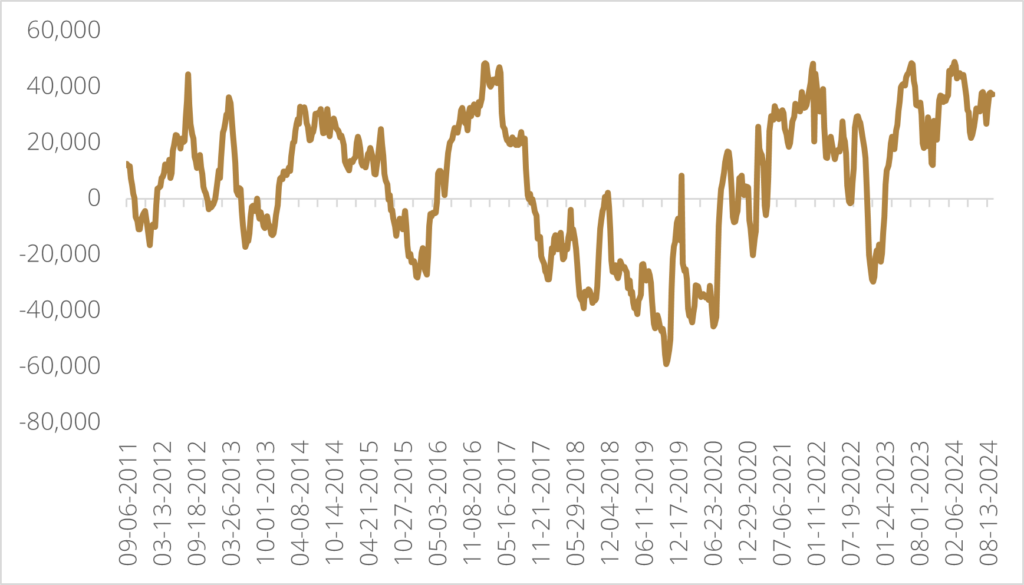

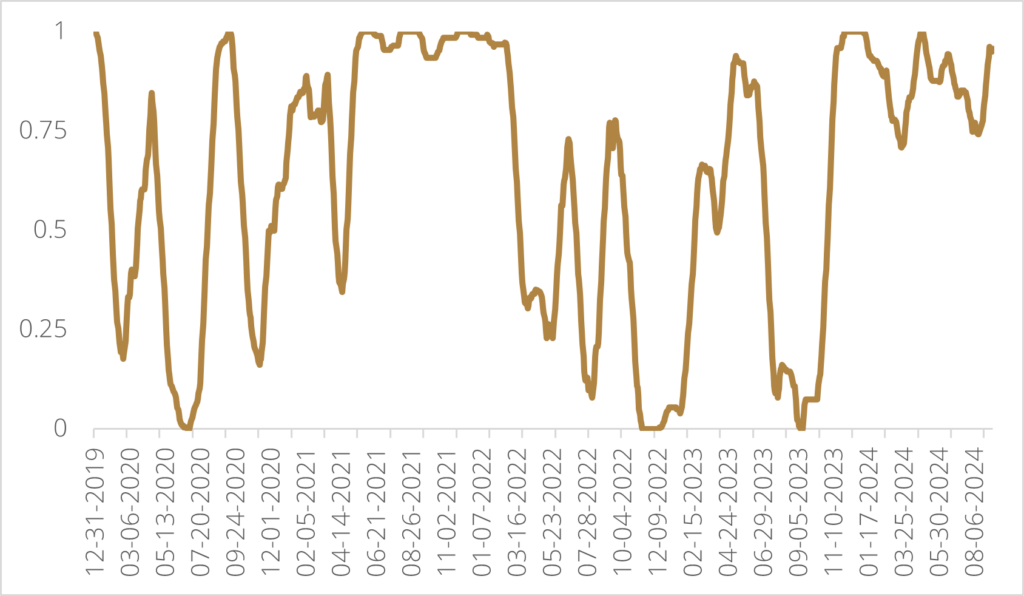

Managed money and speculative positioning for both Arabica and Robusta futures remain elevated, with both markets exhibiting a strong positive trend score.

We continue to remain bullish on both varieties of coffee based on growing demand from China along with supply chain concentration risks that are susceptible to erratic weather patterns. In the short term, we could see somewhat of an easing in prices, as traders are likely to have pulled forward some demand in anticipation of EUDR, and the focus now turns to the new crops and to what extent the excessive heat during the flowering periods will affect yields.

Happy investing!

Scott Smith

Chief Investment Officer

ABOUT THE AUTHOR

DISCLAIMER:

This blog and its contents are for informational purposes only. Information relating to investment approaches or individual investments should not be construed as advice or endorsement. Any views expressed in this blog were prepared based upon the information available at the time and are subject to change. All information is subject to possible correction. In no event shall Viewpoint Investment Partners Corporation be liable for any damages arising out of, or in any way connected with, the use or inability to use this blog appropriately.