From the Desk of Our CIO

Strategic Metal, Strategic Moment: Copper at the Heart of Geopolitical Tensions

After dropping into correction territory earlier this month, U.S. equities have stabilized somewhat, finding some support on the hopes of a less aggressive rollout of wider U.S. tariffs next week and a Federal Open Market Committee (FOMC) meeting where Federal Reserve (Fed) Chairman Jerome Powell downplayed some of the mounting concerns around a slowdown in U.S. growth. Powell communicated during his press conference that the “hard data” in the U.S. economy has been solid, and some of the “soft data” that has reflected rising concerns about future inflation are “outliers.” The FOMC decided to leave interest rates on hold at their monetary policy meeting, with Powell striking a relatively sanguine message around the impact of tariffs on consumer prices being a one-time shift in price levels as opposed to a structural phenomenon; the word “transitory” was even used again! Markets responded favourably to the comments from Powell’s press conference, as well as the announcement that the Fed would be reducing the pace of its balance sheet runoff, which should mitigate some of the risks that the increased supply of treasuries is sucking up too much liquidity.

Looking at the summary of economic projects submitted by FOMC participants paints somewhat of a less rosy near-term outlook. The FOMC downgraded their GDP forecast for 2025 from 2.1% to 1.7%, while also increasing their expectations for core PCE inflation from 2.5% to 2.8%. The median FOMC member continues to expect two interest rate cuts in 2025 (same as in December 2024); however, the composition of those estimates has shifted higher, with eight members (from four in December) now expecting one or no cuts. This is a nuanced shift in FOMC members’ intentions, but it also highlights a divergence in market expectations, with the futures market pricing in roughly two and a half cuts by the end of 2025. Powell may be taking a more optimistic tone on his views towards the impact of tariffs on inflation, but there are subtle shifts underneath the surface that FOMC members are becoming more hawkish on their expectations of future rate cuts.

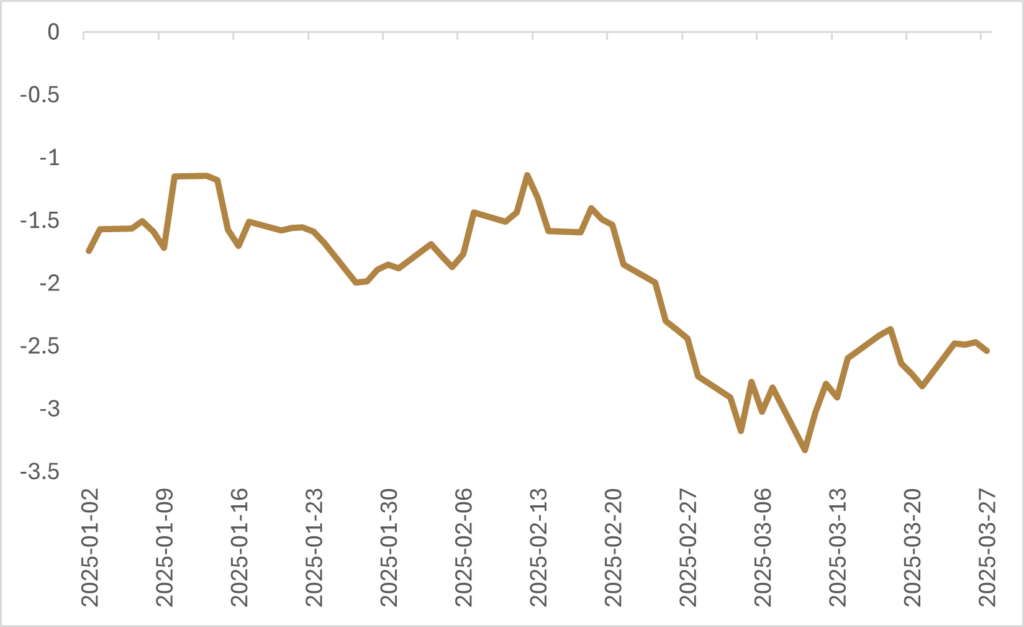

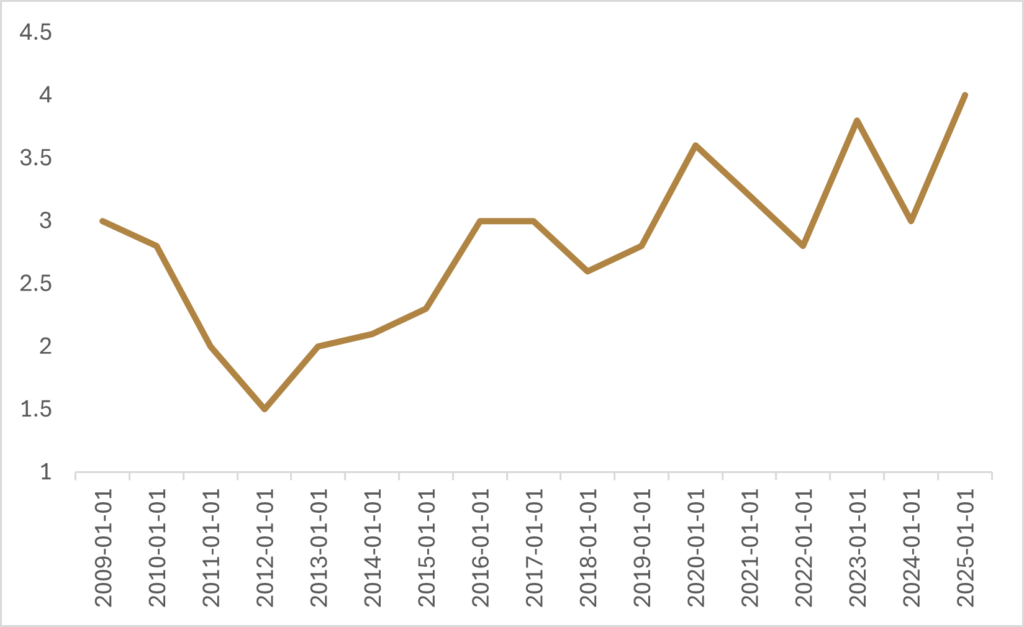

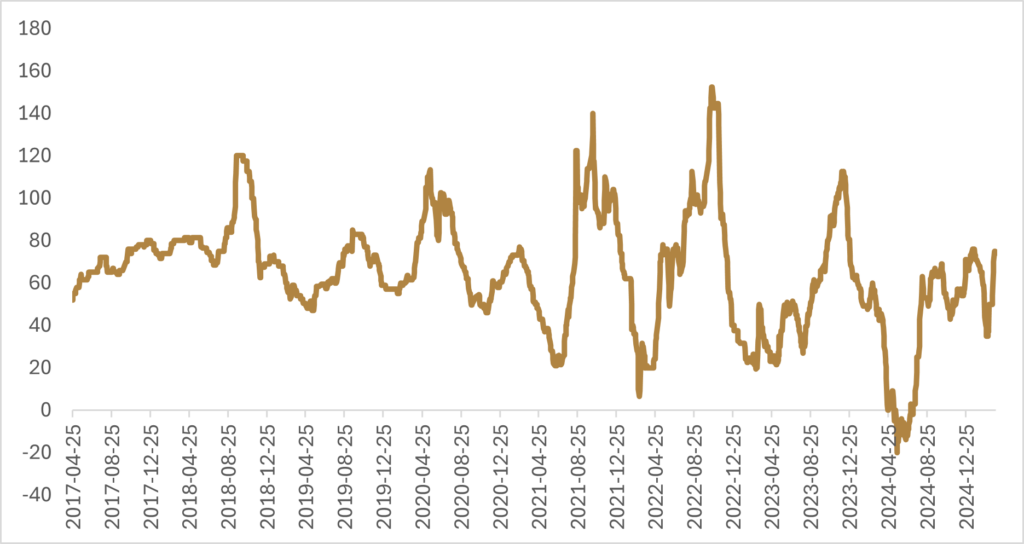

Given all the news headlines, it probably isn’t surprising that that survey data is reflecting elevated levels of uncertainty around the economic outlook. While U.S. equities got a boost that the reciprocal tariffs set to go into effect on April 2nd wouldn’t be sector specific and Trump might give “many” countries a break, the announcement this week of 25% tariffs on automobiles made outside of the U.S dented risk appetite. While trade policy is a constant source of consternation for markets, uncertainty is also reverberating through the U.S. oil patch, a swing from earlier optimism about how deregulation and a “drill baby drill” attitude from the incoming Trump administration would be a boon for U.S. oil producers. The Federal Reserve Bank of Dallas released their quarterly survey of oil and gas firms located in their district this week, and the results were quite pessimistic about the outlook for the industry. The survey results illustrated that the respondents’ outlook toward the future decreased by 12 points to -4.9, while the uncertainty index jumped 21 points to 43.1. Included in the survey were comments from oil and gas executives, with some sounding off that the “administration’s chaos is a disaster,” tariff policy has “immediately increased cost of our casing and tubing”, and that the “threat of $50 oil prices by the administration has caused our firm to reduce its 2025 and 2026 capital expenditures.” The Dallas Fed Energy Survey is another case of a downturn in sentiment due to increased policy uncertainty, and while we haven’t seen this pessimism spill over into hard data in a more meaningful way, the question will be at what point all this uncertainty starts to affect the hard data like factory orders, industrial production, employment, and retail sales.

Although there are reasons to be cautious in this environment, unless we see a meaningful deterioration in hard data, it’s difficult to be extremely bearish at this juncture. Volatility is at relatively subdued levels, U.S. yields are off the highs at the end of last year, the U.S. dollar has been weakening, and we’re seeing expansionary fiscal policy from Germany and China. The potential for fiscal detox in the U.S. and a slowdown in growth may be growth-negative in the short term, but we see this as a reason for portfolios to embrace geographical diversification as global fiscal policy diverges. We’ve highlighted in previous notes the steps that Germany is taking to revitalize its domestic infrastructure through an increase in defense spending, and the potential for a larger fiscal thrust than during reunification has led to stark outperformance in European equities. Though not the same magnitude as the planned fiscal expansion in Germany, China has also ramped up spending plans by setting its 2025 fiscal deficit target at around 4% of GDP, a major departure from the 3% deficit target that China has previously communicated. With U.S. trade policy creating uncertainty around the growth outlook for China, Beijing seems to remain committed to their economic growth goal of 5% this year, communicating that both fiscal and monetary policy can be further expanded if necessary. The top priority for Beijing is to boost household consumption, with the administration outlining a plan to increase support for social wellbeing that includes childcare subsidies and paid leave.

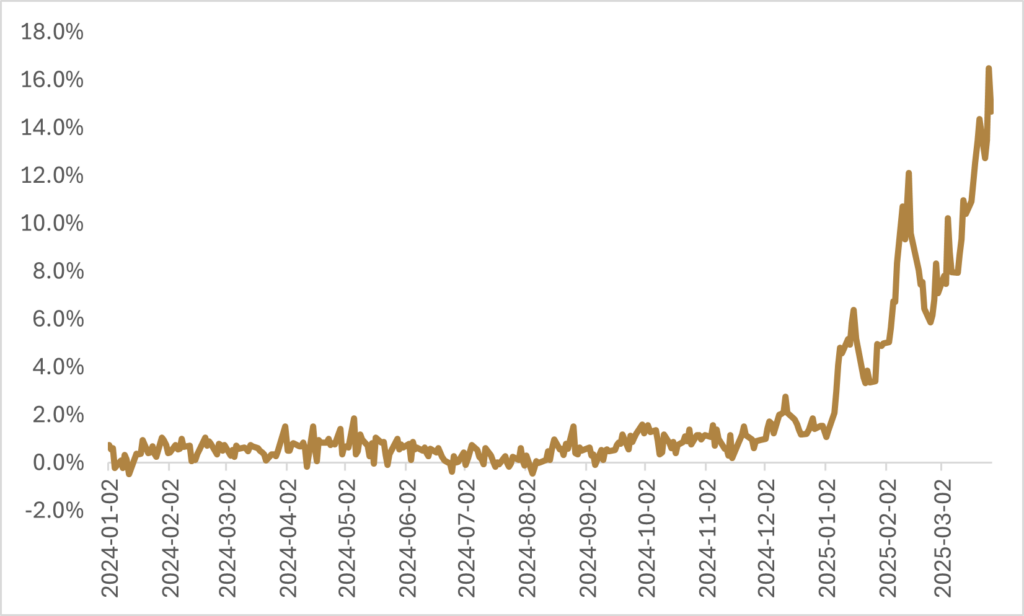

One of the commodities that has been a beneficiary of the expansionary fiscal policy in China has been copper, which is one of the best performing commodities this year, with futures prices rising over 25%. We had written a note in September of last year about how after a pull-back from recent highs earlier in 2024, underlying fundamentals in the Chinese copper market were improving and that copper could be a benefactor of additional fiscal stimulus from Beijing. Premiums paid to take delivery on refined copper into China have stabilized after the negative prices witnessed last summer, suggesting that fundamentals are relatively healthy. While the efforts to boost consumption in China have been a tailwind for copper prices, the potential for the U.S. administration to levy tariffs on copper imports has tightened global supplies. As we wrote about a few weeks ago, the spread between copper delivered on U.S. exchanges and copper delivered on the LME exchange has been pricing in the potential for these tariffs. The increased spread in prices has resulted in traders rushing to ship copper into the U.S. to take advantage of higher prices, hoping to get the copper delivered ahead of any levies. Global metals trader Mercuria has estimated that the dislocation in prices has led to 500,000 tons of copper being routed to the U.S., well above the normal monthly imports of 70,000 tons, tightening the global copper market. However, this physical arbitrage trade got spooked earlier this week when the U.S. administration announced that a decision on copper tariffs could be coming within several weeks, not near the end of the year like had originally been communicated, raising worries that physical copper on route may not make it to the U.S in time before tariffs are put into effect. The market is anticipating that the expedited investigation is likely little more than a formality, with copper prices on the CME continuing to rise versus that of the LME.

In normal circumstances, I’d suggest that the recent runup in price would be short-lived, with these technical factors pulling forward demand resulting in the physical market needing to work through a glut of copper supply down the line. The futures curve on the CME is also in contango and speculative futures positions are well below the highs from last year, both of which aren’t indicating tightness in the short term. Where we are seeing tightness is on the LME exchange, with an inversion in the futures curve happening for contracts in the back half of 2025. China announced last week that it plans to add to its strategic reserves of key industrial metals this year, with Beijing planning to step up purchases of cobalt, copper, nickel, and lithium. The combination of metal moving to the U.S. to hopefully arrive before tariffs along with increased demand from China is leading to the tightness, and we’re seeing speculative positions on the LME increase accordingly. The counter argument to further meaningful upside in the price of copper in the short term is that expectations of electricity demand from artificial intelligence might be getting ahead of itself, along with the recent pivot from the U.S. administration away from renewable power generation to fossil fuels. However, in a world where geopolitical tensions are running high, and regions like China and Europe continue to look to renewables to diversify their energy mix to be less reliant on fossil fuel imports, the medium-term picture for copper prices remains constructive.

Happy investing!

Scott Smith

Chief Investment Officer

ABOUT THE AUTHOR

DISCLAIMER:

This blog and its contents are for informational purposes only. Information relating to investment approaches or individual investments should not be construed as advice or endorsement. Any views expressed in this blog were prepared based upon the information available at the time and are subject to change. All information is subject to possible correction. In no event shall Viewpoint Investment Partners Corporation be liable for any damages arising out of, or in any way connected with, the use or inability to use this blog appropriately.