From the Desk of Our CIO

Mind Your Duration: Navigating Growth, Inflation, & the Fiscal Impulse

It’s been close to a month since the Federal Reserve (Fed) embarked on what is likely to be the start of a rate cutting cycle, lowering the overnight rate by 50bps. While attention was focused on the “jumbo” nature of the interest rate reduction, given the Fed generally adjusts interest rates in 25bps increments, the 50bps move basically caught up to market expectations for what had been anticipated over both the July (roughly 15bps of cuts) and September (roughly 35bps of cuts) monetary policy meetings. What was arguably the most interesting takeaway from the September meeting was that the projections by Fed members for where the overnight rate will settle in the long run continues to rise. In December of 2023, the median Fed member projected that the long run overnight rate (known as the neutral interest rate) would be 2.5%, but this estimate from Fed members has steadily increased throughout 2024, with the September estimate rising again to 2.9%. Forecasting the neutral rate of interest is fraught with estimation errors even for Fed members; however, it is telling that expectations for where long-term interest rates will settle has been increasing.

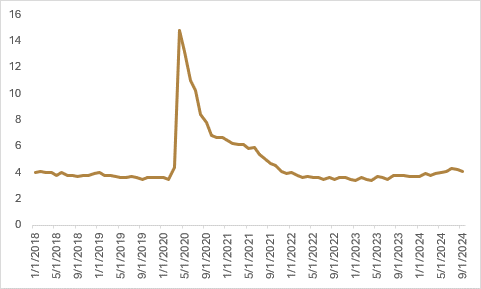

Since the September policy meeting, U.S. fixed income has struggled, with longer-term interest rates feeling the brunt of the pain. 30-year bond futures have fallen by a little over -6%, while 10-year bond futures are down just over -2%. This is not just a result of a more hawkish long-term view from Fed members, but the economic data has also come in hotter than anticipated, reinforcing the view that the Fed is likely cutting into a growth “speedbump” and not a “pothole.” The September payrolls report surprised to the upside, and the household survey showed that the unemployment rate for September ticked down to 4.1%. While the labour market has been cooling throughout 2024, it does not appear that, in the short term, the U.S. labour market is at risk of freezing over.

With inflation easing over the last 18 months, the Fed has turned its attention to the other side of its dual mandate, using a softening labour market as the impetus to embark on a rate cutting cycle. The question that financial market participants will be grappling with now is: if the U.S. economy isn’t in danger of entering a recession, how many cuts will the Fed be able to get in before their attention must come back to inflation? If the Fed is indeed cutting into a growth speedbump, will they be able to linearly reduce interest rates to get to what is deemed as the neutral rate of interest (i.e., soft landing), or will global growth pick up at a rate where inflation starts to rise, and the Fed needs to pause their rate cut cycle (i.e., “no landing”)?

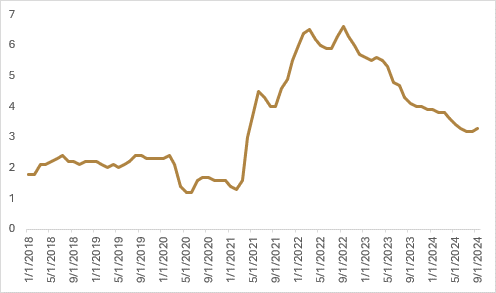

The “no-landing” camp received some validation last Thursday, as consumer prices for the month of September in the U.S. came in warmer than anticipated. While headline inflation eased on a year-over-year basis to 2.4%, this was less than the 2.3% that had been anticipated by economists. Furthermore, core inflation (ex-food and energy) increased on a year-over-year basis to 3.3%, hotter than the 3.2% reading in August. The risk of a resurgence in inflationary pressures is likely to dominate the market’s view of near-term economic data points, especially as we get closer to the U.S. election in early November. Truflation’s real-time reading on U.S. inflation has bounced from 1.5% in September to its current reading of 2.2%, providing further evidence the “soft-landing” scenario may be challenging to engineer if there is a surge in demand. After the Fed’s monetary policy meeting in September, market expectations were for the Fed to cut another three times in 2024 (50bps at one meeting and 25bps at another meeting), and that by September of 2025, the overnight rate would be at the Fed’s perceived long-term neutral of 2.9%. After the stronger than anticipated economic data, markets are now expecting a little under two cuts (44bps) by the end of 2024, with the overnight rate bottoming at 3.3% in January of 2026.

With the U.S. economy continuing to show robustness, this has led to higher U.S. bond yields and a higher U.S. dollar, as market participants are expecting other global central banks (e.g., Bank of Canada, Bank of England, European Central Bank) to embark on a more aggressive easing path, given the relative weakness of their economies. While German fixed income has also hit a speed wobble over the last month, the upward shift in yields has been much less pronounced than the U.S. yield curve, with German 10-year bond futures only falling by a little under -1%. This highlights that even in an environment where global interest rates are expected to move lower in a uniform fashion, it still pays to have a globally diversified fixed income basket.

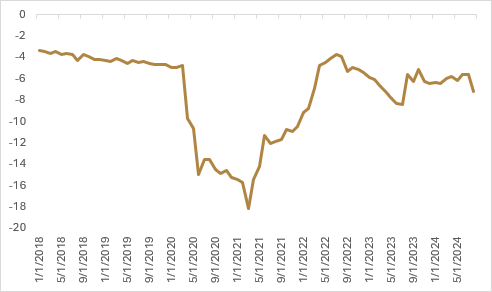

While a lot of market attention has been focused on global monetary policy in the face of the potential for a resurgence in inflation, fiscal policy has taken somewhat of a backseat. The newly-formed French government led by Prime Minister Michel Barnier unveiled a new budget last week to tackle its public debt challenges, aiming to narrow the government deficit from 6.1% of GDP this year to 5% in 2025. The proposed budget will aim to deliver almost 61 billion euro of savings, with two-thirds of the amount coming from spending cuts and the rest coming from tax hikes. Barnier still has a long way to go in appeasing both the left-leaning New Popular Front and the right-leaning National Rally, with Bloomberg noting the challenge will be to “find a balance of measures that are acceptable enough for Le Pen to refrain from allying with the left to bring down the government.” With the amount of ink that tends to be spilt around fiscal strain in Europe, there has been much less focus on the U.S. fiscal deficit, which is currently running at -7.2%, and how impactful it has been at insulating U.S. economic growth. The optimistic view on the U.S. fiscal situation is that widening deficits have in part been due to investment in industrial policy through the IRA and CHIPS Act, but the relative size of the U.S. budget deficit remains in stark contrast to that of global peers.

This is all to say that, in the short term, market participants may be intently focused on how the high-frequency economic data points will affect the Fed’s rate cutting cycle. However, the more economically impactful data points on which to focus (in our view) will be how the global fiscal situation unfolds, particularly in the U.S. with the upcoming presidential election in a little under a month. We continue to feel that a shift towards populist governments will make it harder for governments around the globe to meaningfully rein in budget deficits, which will put upward pressure on longer-term bond yields and cause duration in fixed income portfolios to suffer. Ongoing fiscal support to “reindustrialize” and diversify supply chains makes a good case for a meaningful allocation to broad commodity markets, as our view is that the bigger risk for investment portfolios is upside surprises to nominal growth and periodic resurgence in inflationary pressures due to deglobalization.

Happy investing!

Scott Smith

Chief Investment Officer

ABOUT THE AUTHOR

DISCLAIMER:

This blog and its contents are for informational purposes only. Information relating to investment approaches or individual investments should not be construed as advice or endorsement. Any views expressed in this blog were prepared based upon the information available at the time and are subject to change. All information is subject to possible correction. In no event shall Viewpoint Investment Partners Corporation be liable for any damages arising out of, or in any way connected with, the use or inability to use this blog appropriately.