From the Desk of Our CIO

The Warsh Reckoning: A Liquidity Reset or a Temporary Repricing?

The nomination of Kevin Warsh as the next Chair of the Federal Reserve landed with more force in financial markets than many anticipated. Expectations heading into the decision were that any incoming Chair would lean more dovish than Jerome Powell, reflecting the Trump administration’s sustained pressure on the Fed to lower interest rates. Against that backdrop, Warsh’s nomination proved a surprise catalyst for a broad repricing across bonds, currencies, and commodities. The U.S. yield curve steepened, the dollar strengthened, and precious metals sold off. This was not because markets suddenly feared higher short-term rates, but because investors began reassessing how Warsh’s confirmation could alter the future size, composition, and role of the Fed’s balance sheet, given his long-standing criticism of quantitative easing (QE).

At issue is whether his appointment marks a genuine shift toward a smaller-footprint central bank, where the private sector absorbs more duration risk, or whether the reaction reflects a temporary adjustment constrained by political, economic, and financial realities.

Early in the process of selecting the next Fed Chair, it appeared that Kevin Hassett was the frontrunner to succeed Jerome Powell. That narrative faded as it became clear that his proximity to the Trump administration, as Director of the National Economic Council, would raise questions around perceived Fed independence — a constraint that ultimately mattered more than policy alignment. There was a short period when it looked as though BlackRock executive Rick Rieder would emerge as the frontrunner, given his outright dovish tone on both interest rates and long-term monetary policy. However, after reports surfaced that Rieder had donated to Republican opponents of Donald Trump, Warsh re-emerged as the likely nominee. The decision was leaked Thursday night and ultimately formalized Friday morning.

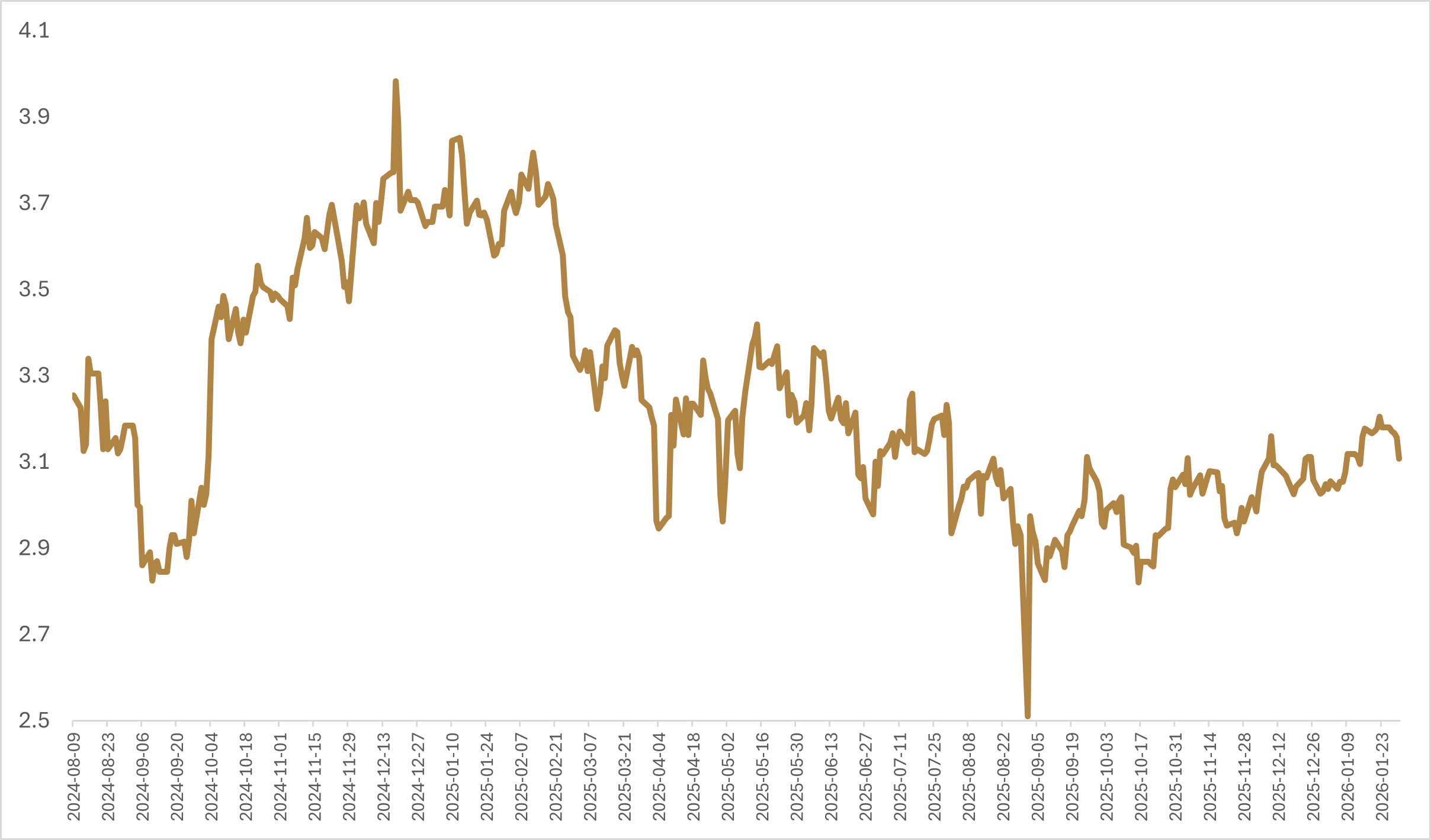

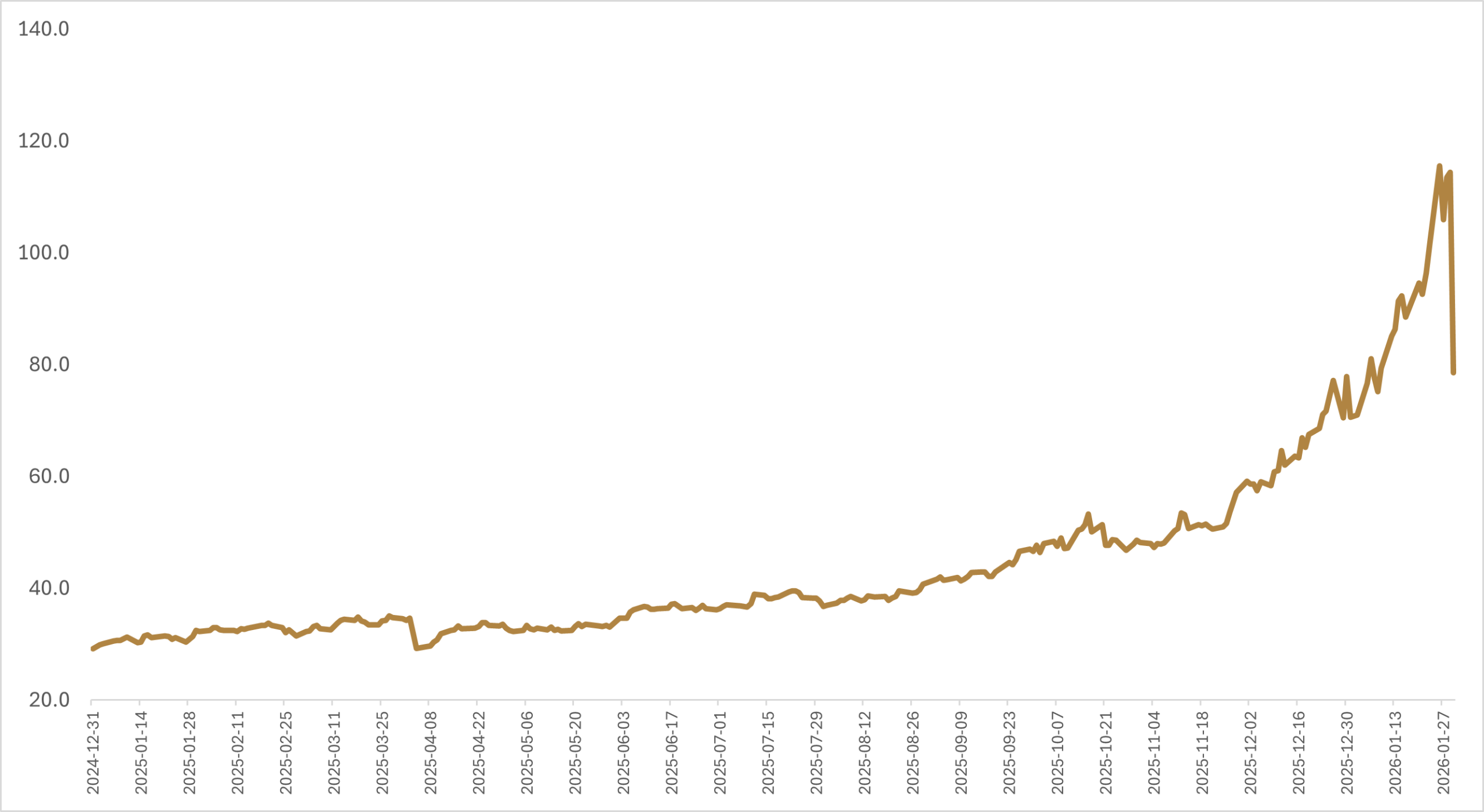

Markets initially interpreted the nomination as hawkish, leading to a steepening of the U.S. yield curve, with short-term rates falling and long-term rates rising. This steepening hit long-duration assets, corresponding with a dramatic sell-off in precious metals and a resurgence in the U.S. dollar. It was a historic day for silver, with front-month futures down nearly 40% at the intraday lows before finding support and ultimately finishing down 25%. Other metals also hit air pockets, though not to the same extent as silver, with gold and copper finishing the day down 11% and 5%, respectively.

While Warsh’s nomination was the initial spark, the reinforcing feedback loop of leveraged speculators being stopped out — including leveraged ETFs needing to rebalance delta exposure — amplified the sell-off. Even with the liquidity cascade in the metals complex, U.S. equities finished the day off the lows and were down just 0.5%. And despite the historic daily declines in precious and industrial metals, silver remains up 11% year to date, while gold and copper are up 8% and 4%, respectively.

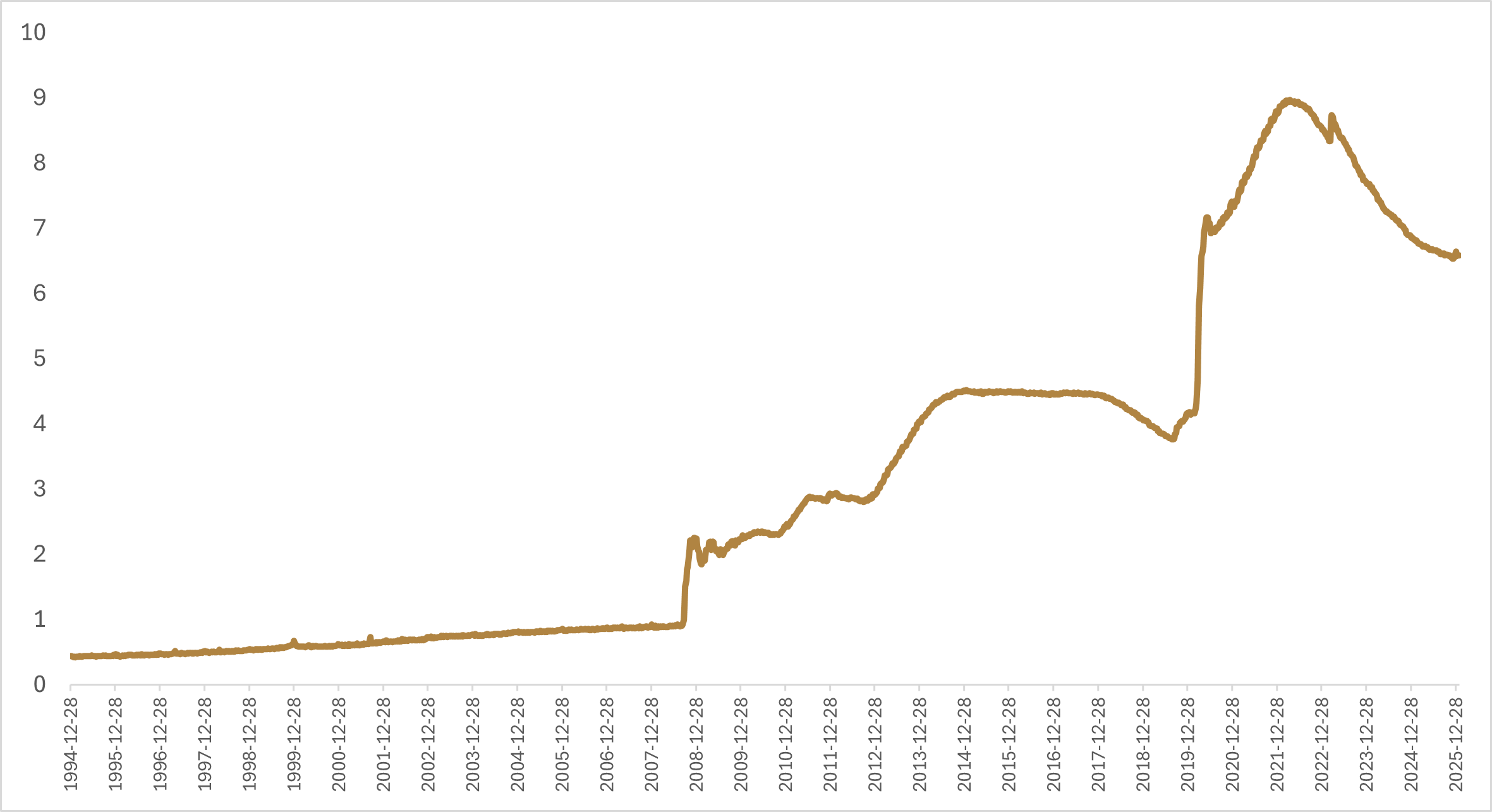

Ultimately, the market reaction was less about near-term policy rates and more about what Warsh might do with the Fed’s balance sheet. Historically, Warsh leaned hawkish in the aftermath of the Global Financial Crisis and, in hindsight, placed greater weight on inflation risks than on the disinflationary forces that ultimately prevailed. While he supported emergency measures initially, he became increasingly opposed to subsequent rounds of QE, viewing them as a distortion of price discovery and a blurring of fiscal and monetary roles. This misalignment with other board members and the prevailing policy direction ultimately led him to step down from the Board of Governors in 2011. He remained vocal in his criticism of Fed policy for years afterward, including during the 2024 cutting cycle, when he argued that rate cuts risked undermining inflation credibility.

Following Trump’s re-election in 2024, Warsh’s tone shifted. He began advocating for lower policy rates, citing supply-side forces, AI-driven productivity, and the risk of overtightening. With inflation still above the Fed’s target, this pivot has raised questions about whether the change reflects pragmatism or positioning for the role of Chair.

Both interpretations matter. It is entirely possible that Warsh is less ideological than his reputation suggests and that, once in the role, consensus-building will prove more difficult than outright criticism of the Fed’s operations. However, if Warsh does succeed in running a smaller-footprint Fed with less balance-sheet activism and a preference for hard-money principles, markets will need to reprice existing risk premiums.

This is where markets are currently focused. The dominant risk being priced is not the level of short-term rates, but the structure of the Fed’s balance sheet. A continuation of quantitative tightening, or a deliberate shift toward holding fewer long-duration assets, would push more duration into the private sector. With increased supply comes price adjustment. That dynamic is consistent with the move observed on Friday: a steeper curve, a stronger dollar, and weaker metals. If Warsh is able to realize his view of lower short-term interest rates alongside reduced balance-sheet duration, the effect would likely be to shift asset price inflation toward real-economy inflation, requiring markets to adjust to a new liquidity framework.

While there is a coherent framework that has unsettled long-duration assets and increased the risk to our bullish 2026 outlook, it remains too early to determine whether positioning should change meaningfully. Expectations are clearly different than they would have been under Hassett, Rieder, or a continuation of Powell. Paradoxically, financial conditions could tighten if short-term rates fall while the private sector is forced to absorb more duration through quantitative tightening or balance-sheet reconfiguration. That is not an outcome markets or policymakers are likely to accept indefinitely. If long-term rates move too aggressively, there is a high probability the process would be slowed or partially reversed. This is why implementation matters more than rhetoric, and while the Fed is “independent,” political considerations inevitably influence senior appointments.

One important constraint is the Federal Open Market Committee (FOMC), which consists of 12 voting members. While Warsh would control the agenda and messaging, he would still require six additional votes to secure a majority. Although there have been recent dovish dissents in favour of further rate cuts, the current mix of voters is fairly balanced, with many emphasizing data dependence — an approach Warsh has criticized in the past. Consensus around continued rate cuts may prove challenging unless economic data deteriorates meaningfully or inflation continues to ease, and wholesale changes to balance-sheet policy would likely face even greater resistance.

Beyond internal FOMC dynamics, a smaller Fed balance sheet with less duration may conflict with the administration’s affordability priorities. Trump stated last week at a cabinet meeting that supply-side reforms to lower home prices are not on the agenda, indicating a preference for rising home prices to benefit existing owners. That leaves lower mortgage rates as the primary lever for housing affordability, yet mortgage rates are tied to the long end of the yield curve, not the overnight rate. A persistent steepening of the curve would therefore undermine mortgage affordability — an outcome the administration is unlikely to tolerate for long. Such a steepening would also likely coincide with a stronger U.S. dollar, running counter to the administration’s preference for a weaker currency to improve manufacturing competitiveness.

This constraint-based framework raises the possibility of a familiar pattern. Scott Bessent sharply criticized the Biden administration’s reliance on short-dated Treasury issuance while outside government, only to continue the same approach once in office as Treasury Secretary, constrained by market realities. Warsh may face similar limits regarding the size and duration of the Fed’s balance sheet.

For now, it remains premature to make wholesale allocation changes based on a single appointment. The FOMC still consists of eleven other voting members, and institutional inertia remains powerful. That said, Warsh’s nomination meaningfully shifts the distribution of outcomes relative to what markets had been expecting under Hassett, Rieder, or a continuation of Powell. In fixed income, this reinforces our preference to remain underweight global duration until the yield curve steepens further and term premia are more clearly priced. In equities, the risk lies less in near-term earnings and more in valuation sensitivity, leaving long-duration growth assets more exposed than quality and income-oriented exposures. While precious and industrial metals may experience near-term volatility as positioning adjusts, the broader structural case tied to geopolitics, supply constraints, and a more multipolar world remains intact. In that sense, the Warsh steepener may prove less a regime change than a stress test — with forced repricing creating opportunities for patient capital willing to look beyond the noise and selectively add to existing thematic exposures.

Happy investing!

Scott Smith

Chief Investment Officer

ABOUT THE AUTHOR

DISCLAIMER:

This blog and its contents are for informational purposes only. Information relating to investment approaches or individual investments should not be construed as advice or endorsement. Any views expressed in this blog were prepared based upon the information available at the time and are subject to change. All information is subject to possible correction. In no event shall Viewpoint Investment Partners Corporation be liable for any damages arising out of, or in any way connected with, the use or inability to use this blog appropriately.