|

5. Positioning

Our house view, which we incorporate into separately managed portfolios, but does not influence our pooled fund model, carries forward the framework that worked through the first six months, with two conditional layers.

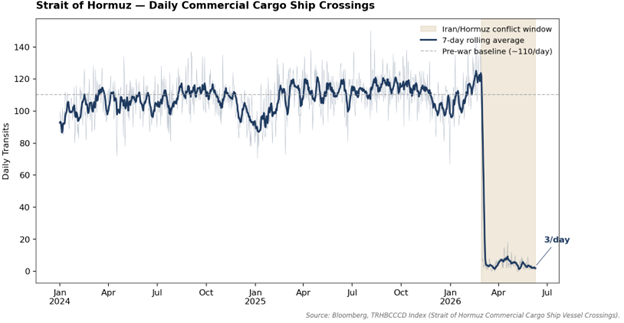

We remain overweight commodities. The structural case is reinforced by the multipolar world where commodities will have a structural geopolitical risk premium embedded as nation states look to fortify commodity supply chains. The near-term tactical pullback we expect as the worst-case Hormuz scenarios fade is an opportunity to add to existing positions or establish new ones at improved entry levels.

We remain overweight international equities relative to the U.S. in common-currency terms. The conditional caveat is the U.S. dollar. A meaningfully more hawkish Fed move alongside USD strength would push us toward a more neutral geographic stance, since the common-currency tailwind that has driven the year-to-date international lead would partially reverse.

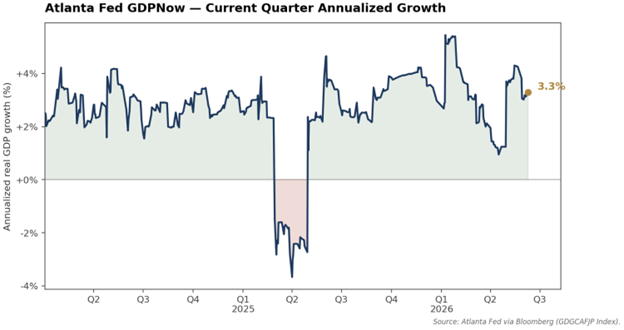

Within U.S. equities, we continue to tilt away from cap-weighted exposure and toward quality and yield factors. Businesses that generate cash and return it to shareholders, rather than businesses that consume cash to fund AI infrastructure, are the right exposures heading into a back half defined by two-track tightening of financial conditions.

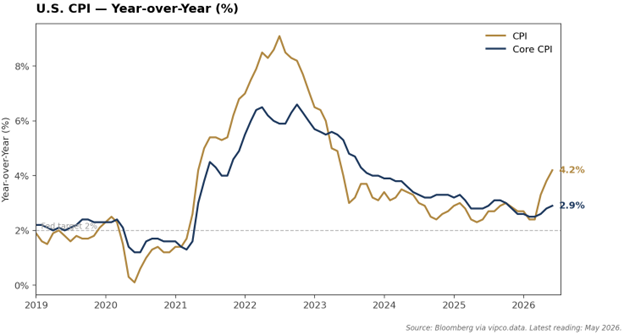

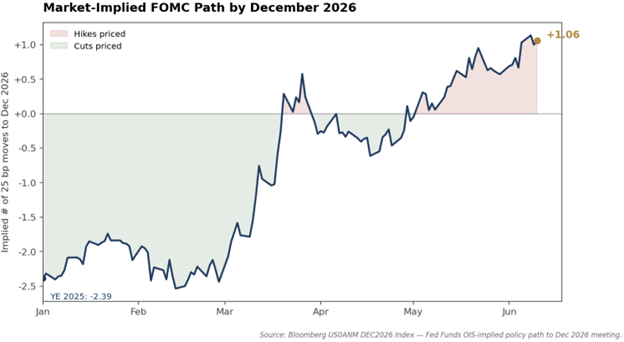

Fixed income remains underweight in aggregate. The conditional move is long duration. If the Fed pivots hawkish and the real economy slows in response, the curve will likely flatten or invert, and long duration becomes the cleaner recession hedge. While we’re seeing early signs of curve flattening, neither condition is fully locked, and the June FOMC meeting and dot plot are important signals to watch.

Our discretionary views don’t factor into portfolio construction for our pooled funds but can be helpful as investors think about their holistic portfolio construction. The Viewpoint pooled funds are rules-based and adaptive to the evolving market environment, adjusting capital allocations based on volatility, correlations, and in the case of the multi-assets, additional quantitative overlays.

For the Viewpoint Diversified Commodities (VCOM) strategy, the most meaningful capital allocation change through the first half has been a large reduction in exposure to the energy sector, with most of the change concentrated in thermal coal. Heading into the start of the year the VCOM strategy was overweight energy relative to historical model averages, and after the breakout of the Iran war and the pop higher in both price and volatility, the strategy reduced capital exposure to keep the risk allocation from energy markets stable, taking profits on the price rise. The capital pulled out of energy has been redeployed across the remaining sectors, with the largest increases accruing to livestock and grains. The shift is signal driven rather than discretionary, with the strategy responding mechanically to the volatility re-rating in energy through the first quarter. The result, however, leaves the strategy well positioned for any weather or fertilizer-related spillover from Hormuz in the back half of 2026 through its exposure to agriculture.

For Viewpoint Enhanced Global Equity Yield (VEY), the strategy quantitatively screens for quality and shareholder yield characteristics, so it already tilts away from pure market cap weightings. Within the screened opportunity set, the strategy then uses a risk parity approach to determine capital weightings so that each equity sector (as well as individual equities within the sector) contributes the same amount of risk to the portfolio. Year-to-date, as volatility and correlations have shifted, the strategy has added the most capital to the energy and utilities sectors, while decreasing capital exposure to materials and financials. While the strategy has added slightly to the tech sector year-to-date, information technology sits at 8.3%, a material underweight relative to the 32% weighting in the global equity (ACWI) benchmark.

Viewpoint Global Multi-Asset (VMA) has materially de-risked through the first half of 2026, with strategy leverage starting the year at 158%, moving close to 250% ahead of the Iran conflict, and then de-risking back down to 124% today. On a normalized basis, the active capital allocation tilts have been into commodities, funded by a reduction in nominal rates as time-series momentum signals shifted away from government bonds — with U.S. and Emerging Market nominal bonds the two largest sub-allocation reductions of the half. On a geographic basis, Japan has emerged as the relative winner, holding its capital allocation relatively steady as U.S. and Emerging Market exposures came down more aggressively.

The Viewpoint Enhanced Global Multi-Asset strategy has de-levered even more substantially than VMA, which is a function of having a higher volatility target than VMA. Gross leverage of the strategy has moved from 382% to 269%, decently below the historical model average. Both multi-asset strategies are now in a more defensive position than historical model averages, responding to the higher volatility across financial markets. On a normalized basis, the active rotation has been similar to VMA, with a large capital rotation into commodities and inflation-linked rates, funded predominately by a reduction in international nominal sovereign bonds. Within the quantitative overlays, the commodity long/short overlay has been adding to agricultural commodities like canola and cotton, but also to energy products like WTI and Dutch Natural Gas. This capital allocation is obviously different than the behaviour of the VCOM strategy, with the long/short overlay harvesting trend signals to increase its exposure to energy, while the portfolio construction of VCOM harnesses a mean reversion tilt within the risk parity framework. |