From the Desk of Our CIO

Metal Mayhem: Tariff Uncertainty Permeates Through Commodity Markets

Hardly a day goes by without a new headline surrounding U.S. trade policy, with the result being an ever-increasing list of potential tariffs on U.S. trading partners. The next few weeks are unlikely to offer any reprieve from headline-induced shocks, with the delay of across-the-board tariffs originally imposed on Canada and Mexico set to expire on March 4th, and the current indication from the White House is that they are set to go ahead. Even if there is a further delay or deal to be reached prior to next Tuesday, 25% tariffs on steel and aluminum imports from all nations are set to go into effect on March 12th.

Canada is the United States’ biggest supplier of primary aluminum and steel; however, the presidential order to place 25% levies on all imported aluminum and steel did not include any exemptions for trading partners. The exclusion of exemptions means that the ability for substitution would remain somewhat limited in the short term to only what the United States produces itself. However, over the longer term, the goal would seemingly be to revive both the aluminum and steel industries in the U.S. and increase domestic production of these strategically important metals. Net imports of aluminum in the U.S. amounted to more than 80% of consumption in 2023, meaning that it’s likely the American consumer would feel the brunt of the tariffs through an increase in prices of imported aluminum in the short term. Unsurprisingly, there may be room for deal making ahead of the March 12th deadline, with Trump having suggested Australia could be granted an exemption due to the country’s import of U.S.-made aircraft. Given the U.S. imported only $273 million from Australia in 2024, an Australian exemption wouldn’t provide much relief to U.S. consumers, but it does create some optimism around the potential for other nations to negotiate in a similar fashion.

While the goal of imposing tariffs on steel and aluminum imports into the U.S. to protect the domestic manufacturing industry seems relatively straightforward, when Trump implemented similar tariffs during his first term, it didn’t necessarily produce the desired outcome. Primary aluminum production did increase from 2018 to 2019 during the initial round of tariffs on steel and aluminum, but the U.S. lost manufacturing jobs during this period and production capacity hardly budged. Since the U.S. lifted their tariffs on Canadian steel and aluminum in May of 2019 after the successful negotiation of USMCA, primary aluminum production in the U.S. has slumped by almost 40%. As such, it is possible the Trump administration may not be as open to negotiating on these critical industry tariffs, if the feeling is that they’d like a “do-over” from their last kick at the can.

For Canadian producers of steel and aluminum, the best case would be if the endgame for the Trump administration was to specifically target subsidized Chinese-manufactured steel and aluminum, and the collateral damage for other traditional allies that produce these metals can be negotiated away with some targeted dealmaking. Subsidized Chinese steel and aluminum have not just been a headache for the United States; Canada already put its own 25% tariffs on Chinese-manufactured steel and aluminum last October, citing similar concerns about overcapacity. Kate Kalutkiewicz, Senior Director for International Trade Policy at the National Economic Council during Trump’s first term, recently said, “The North American economic relationship is one of the most, if not the most, important relationships in the world.” Therefore, if the U.S. policy goal is to reduce foreign dumping and secure the North American economic relationship, then it seems as if there could be an avenue to at least avert some of the more sweeping tariffs on Canadian goods, including steel and aluminum.

If the policy endgame is not to necessarily secure the North American economic relationship but rather a focus on utilizing tariffs to increase government revenue, then the economic ramifications for Canada in the short term become more challenging, as it will be harder to negotiate given Canada’s reliance on the United States as a trading partner. As I wrote last week, the budget resolution that is in the process of making its way through Congressional chambers allows for up to $4.5 trillion in revenue reduction due to an extension of the tax cuts Trump put in place during his first term, while also incorporating $2 trillion in spending cuts to offset some of the lost revenue. With the administration intently focused on the budget deficit and borrowing costs as proxied by the 10-year Treasury yield, the policy thrust from an imposition of sweeping tariffs could be a short-term boost to government revenue. The Tax Foundation, the U.S. nonpartisan group, has estimated that if Trump were to enact all his outlined tariff proposals, government revenue would be raised by just over $1.5 trillion over the next 10 years. This, combined with $2 trillion in spending cuts, would get close to fully funding the extension of Trump’s tax cuts. The Tax Foundation noted that this estimate is using a conventional method of assuming trade flows were to continue as normal, and that government revenues would likely be closer to $1.4 trillion over the next 10 years when factoring in how tariffs shrink U.S. GDP. The dynamic revenue estimate will also shrink further if foreign countries retaliate with their own tariffs, specifically for countries that are large importers of U.S. goods.

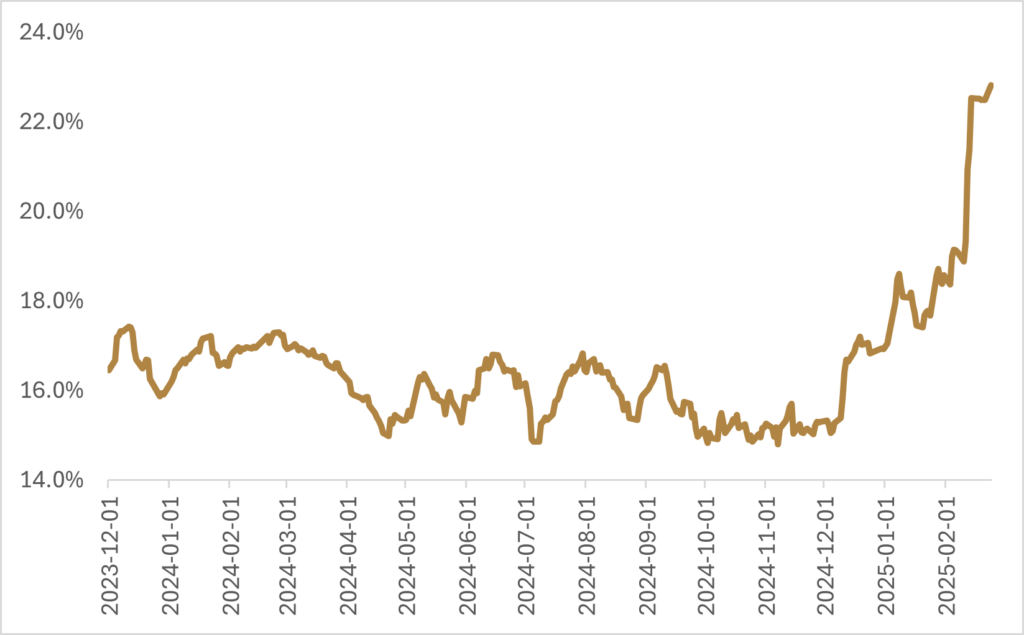

Financial markets have been relatively sanguine around the tariff situation over the last few weeks, with market participants viewing the threat of tariffs as a negotiating tool rather than a hinderance on global trade flows. International equities have been outperforming U.S. equities, while the Canadian dollar has strengthened against the U.S. dollar since the beginning of February. Commodity markets have been less optimistic around the potential for tariffs on critical industries, with various markets starting to price in a higher probability of announced (and unannounced) tariffs. The aluminum futures market is interesting, since both the CME (U.S.) traded contract and the LME (U.K.) traded contract have similar global delivery mechanisms, and the contract reflects the duty-unpaid price of the metal. Both the CME and LME contracts for aluminum futures are up marginally in February (+1-2%). However, the contract that tracks the duty-paid price of aluminum delivered to the U.S. Midwest has been on an upward swing, reflecting that producers are becoming increasingly confident that additional tariffs on aluminum into the U.S. will be applied.

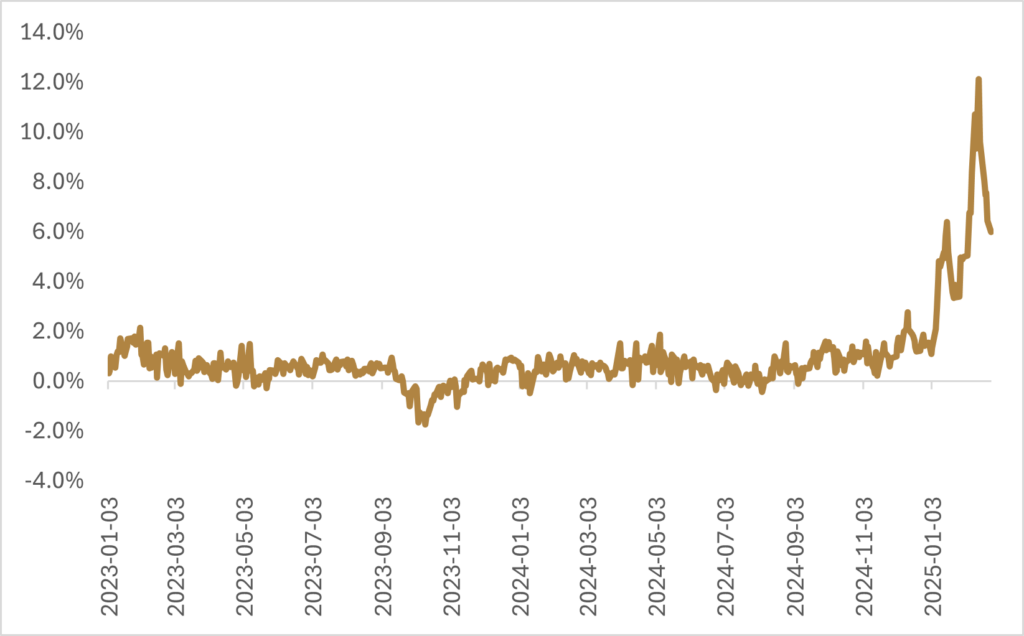

A similar situation is transpiring in the copper market, where market participants have started to build in a premium to CME copper futures relative to LME copper futures, despite there being no tariffs currently announced on copper imports into the U.S. The CME copper contract is slightly different than the aluminum contract in that the copper contract is a duty-paid contract, so the price for CME copper can be directly compared to the LME copper contract, which is duty-unpaid when analyzing potential tariff concerns. While these examples of different delivery point prices for industrial metals aren’t necessarily predicting that the tariffs will be going ahead, they do suggest that producers are paying up for near-term deliveries of these metals to help hedge against some of the policy uncertainty that we’re currently witnessing.

Regardless of how things evolve over the next week, the uncertainty around U.S. trade policy has begun to galvanize new trading coalitions. The German election over the weekend illustrated this effect, with the next German Chancellor, Friedrich Merz, saying the priority of the soon to be formed coalition will be to strengthen Europe as quickly as possible to achieve independence from the U.S. Closer to home, Nova Scotia has put forward their intentions to help reduce interprovincial trade barriers by allowing goods and services to be sold into Nova Scotia without the need for further testing or additional regulatory approval, provided that other provinces and territories pass similar legislation. Ottawa has estimated that eliminating barriers to internal trade could potentially add up to $200 billion to the Canadian economy, more than making up for the hit the Canadian economy would take due to across-the-board tariffs on Canadian imports.

Happy investing!

Scott Smith

Chief Investment Officer

ABOUT THE AUTHOR

DISCLAIMER:

This blog and its contents are for informational purposes only. Information relating to investment approaches or individual investments should not be construed as advice or endorsement. Any views expressed in this blog were prepared based upon the information available at the time and are subject to change. All information is subject to possible correction. In no event shall Viewpoint Investment Partners Corporation be liable for any damages arising out of, or in any way connected with, the use or inability to use this blog appropriately.