From the Desk of Our CIO

Iran, Midterm Incentives, and the Energy Risk Premium: Not Just an Oil Story

Executive Summary

- My starting point in early 2026 was dovish on major U.S. escalation with Iran.

- Midterms amplify the political cost of higher energy prices

- Iran is not a “quick regime calibration candidate” case like Venezuela.

- Post-SOTU, escalation risk rose – fewer visible affordability reforms increases the temptation to seek “wins” abroad, even if that strategy is historically unreliable for midterm elections.

- Midterm history is a headwind – presidents’ parties usually lose seats and keeping control of both chambers is rare and typically requires exceptional conditions.

- Strategically, “regime change by airpower” is not a realistic template. Iran’s security architecture, especially the IRGC, makes a clean, pro-Western transition unlikely without ground involvement, and there is little appetite for that.

- The nuclear issue looks deferred, not destroyed: the new risk is a North Korea–style lesson—deterrence, not de-escalation.

- This is not just an oil story: Hormuz is also a major LNG chokepoint, so the macro transmission channel runs through both crude and global LNG pricing.

- Viewpoint strategy context: energy remains a practical geopolitical hedge. VEMA’s overlay reduced energy exposure through 2H25, then rebuilt and flipped net long in late January as risk premia re-priced.

Iran, Midterm Incentives, and the Energy Risk Premium: Not Just an Oil Story

For much of 2026 I’ve had a dovish stance on the likelihood of a substantial U.S. military escalation against Iran. With the U.S. midterm elections in November and poor polling on the domestic economy, I assumed the U.S. administration would focus more on domestic affordability than foreign policy. I updated my view after the State of the Union last week when there was a lack of meaningful supply-side housing promises and an absence of any concrete plans to address affordability. The thinking was that there was an increased likelihood the administration would continue to pivot towards foreign policy as a way to gain support ahead of the midterms.

I put out a tweet thread on this topic last week, highlighting the risks to that strategy and that elevated oil prices ahead of midterms could be politically costly, and that Iran (unlike Venezuela) did not appear vulnerable to a rapid internal collapse. Relative to earlier in the year, Iran’s regime had regained some power, protest movements had been contained, and any attempt at decisive regime topple would likely be complex, prolonged, and unpredictable, and require U.S. boots on the ground, something U.S. voters would not support.

My original thesis centered on the U.S. domestic economy. While U.S. midterms function as a referendum on the sitting president’s party, historically the president’s party almost always loses seats, and retaining both chambers of Congress is rare and typically requires exceptional national circumstances. The examples of the rare exceptions are Roosevelt in 1934 expanding the Democratic majority during the depression, Clinton in 1998 winning additional seats due to impeachment dynamics and institutional overreach, and Bush in 2002 gaining seats in the post 9/11 geopolitical environment.

These were extraordinary environments, not repeatable foreign policy templates. The 1998 case is particularly instructive. While NATO later conducted operations in the Balkans, the midterm outcome was primarily shaped by domestic backlash to impeachment, not foreign military action. And while we expect that in a multipolar world conflict will be more frequent, but less significant, a focus on foreign policy is unlikely to reliably reverse historical U.S. midterm gravity.

Following the State of the Union, there appeared to be limited substantive movement on supply-side affordability reforms, particularly housing. If domestic economic messaging is faltering, my view is that the administration could be tempted to lean more heavily on foreign policy achievements to reset the narrative. That raised the probability that geopolitical risk could rise even if it conflicted with traditional midterm incentives.

A full-scale regime change in Iran via airpower alone would be historically unprecedented for the United States. Durable regime change has not been achieved through sustained aerial campaigns without boots on the ground and prolonged stabilization, and there is little domestic appetite in the United States for a ground war in Iran.

Iran’s internal power architecture further complicates any assumption of a clean transition given the state operates through parallel security pillars. The conventional military (Artesh) is oriented toward territorial defense while the Islamic Revolutionary Guard Corps is a parallel military/security/economic power center, created out of the revolution and grounded in ideological regime durability.

Even if leadership changes at the top, the decisive question is whether the security architecture remains coherent and if the IRGC is still controlling the state. Iran has now formed a temporary Leadership Council to assume the Supreme Leader’s duties, and one of its members is Ayatollah Alireza Arafi. If Arafi becomes the clerical face of continuity in the post-Khamenei period, it is likely within a system where the IRGC remains the key power broker underpinning internal security and political stability.

Another name often discussed in succession scenarios is Hassan Khomeini, grandson of the founder of the Islamic Republic. While sometimes described as more pragmatic in tone, any elevation of Khomeini would still represent continuity of the Islamic Republic’s institutional framework rather than a systemic departure from it. Even a comparatively moderate clerical successor would govern within the same constitutional and security architecture, with the IRGC remaining structurally embedded in both politics and the economy.

The most likely scenario is that the Iran conflict resembles the Venezuela situation from earlier in the year. This is unlikely to be a full regime change and more like regime calibration. While there are obviously differences in that the Iranian regime has more levers to impose costs by retaliating against Gulf States and disrupting oil and natural gas flows and production, there is little likelihood of a full democratic regime-change.

Neither Arafi nor Khomeini resembles a clean, Western-aligned regime reset. While both could potentially be someone the U.S. could make a deal with in the short-term, it likely only kicks the can down the road. Much like what happened last year after the 12-day war, and one that is indicative of the new multipolar world where skirmishes occur more frequently.

Despite the successful conclusion of last year’s 12-day war, there were never confirmed reports that Iran’s nuclear capabilities were fully destroyed. At best, they were degraded and disrupted. It is now increasingly clear that those capabilities were deferred, not eliminated. The current unknown is how far down the chain of command the U.S. administration would need to go in order to negotiate with actors less hardline than the prior leadership structure. Even if engagement occurs with the comparatively pragmatic figures mentioned above, without a full regime transition, the structural incentives surrounding nuclear deterrence likely remain intact. A short-term off-ramp, potentially centered on limits to enrichment and ballistic missile activity, may stabilize financial markets over the coming weeks. But it does not necessarily resolve the medium-term deterrence problem.

History suggests that regimes facing repeated external military pressure often conclude that conventional forces are insufficient to guarantee survival. In that context, nuclear capability becomes less an offensive tool and more an insurance policy. The clearest modern example is North Korea, which accelerated its nuclear program under regime-threat dynamics and ultimately secured a deterrent that materially reduced the probability of external intervention. If Iran, or a successor leadership aligned with the existing security architecture, draws a similar lesson, the current conflict may paradoxically strengthen the long-run incentive to pursue a credible deterrent. Absent full regime collapse and systemic political realignment, the nuclear issue risks becoming cyclical rather than conclusively settled. The lesson Tehran may draw is not de-escalation, but deterrence.

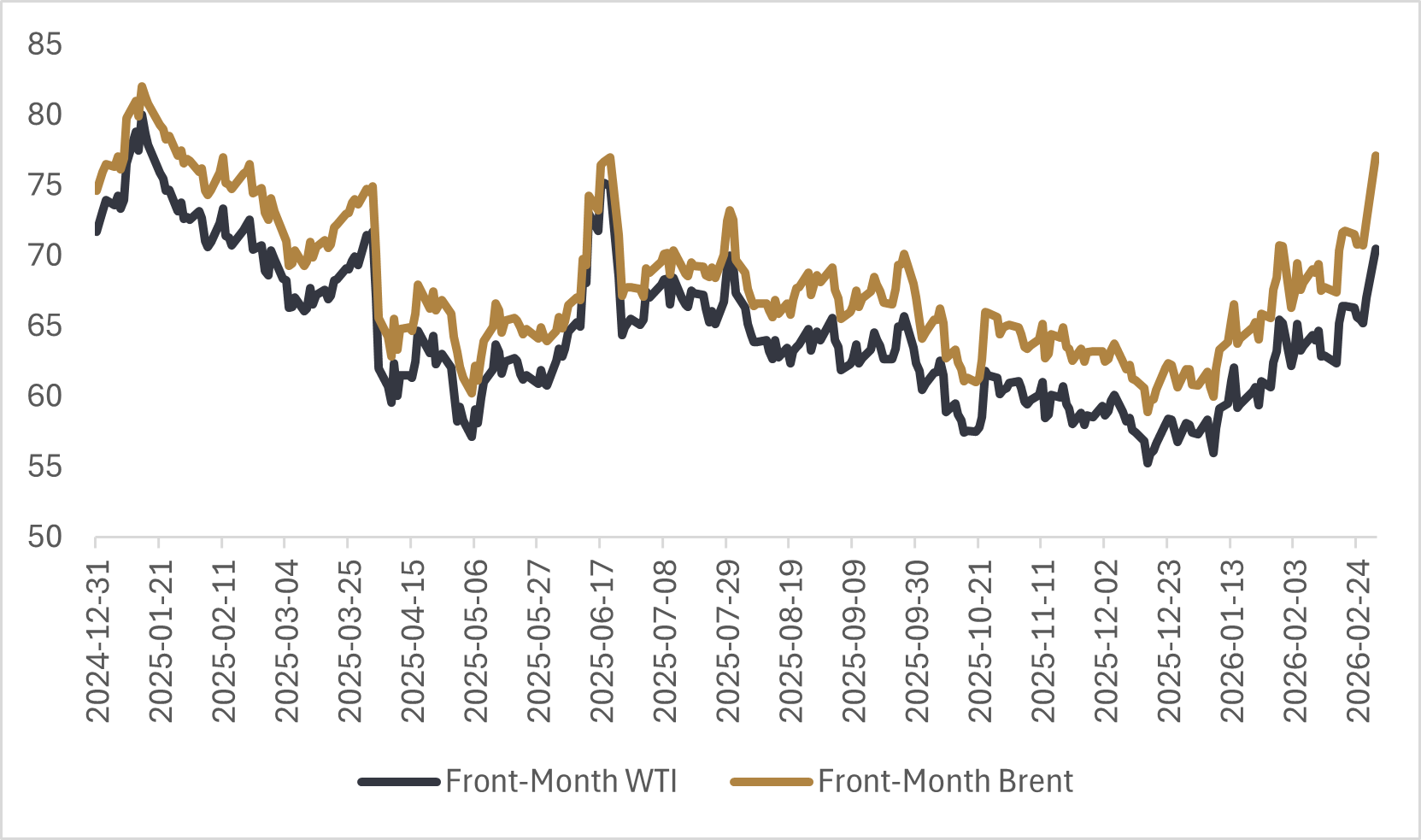

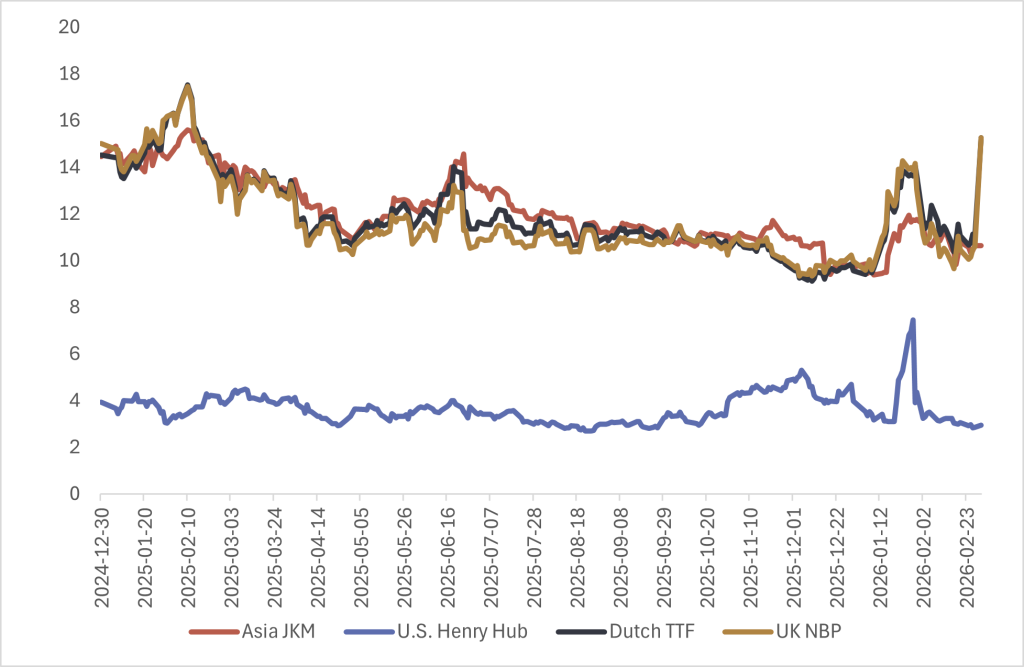

For financial markets, the most immediate concern is the Strait of Hormuz, one of the most critical energy chokepoints in the world. For reference, just over 30% of global seaborne crude oil and 20% of global LNG flows through the straight. While many market participants have been focused on the impact to WTI and Brent crude oil as a result of the escalations in Iran, the effective closure of Hormuz is not just an oil story, it’s also a natural gas and power generation cost story.

And while both WTI and Brent have responded with upside price spikes (+6% respectively at the time of writing), other global energy prices have seen sharper upside moves. With Qatar shutting down LNG production amid attacks on its operating facilities, utilities are scrambling for alternative power sources. Dutch and UK natural gas prices have surged 35% and 40% respectively, while front-month Rotterdam Coal futures are up 12% as many utilities look to switch from gas to coal.

Our base case is that there is an offramp negotiated in the time frame of weeks, but that doesn’t rule out a continued rise is energy risk premia, especially if retaliation continues to target shipping or regional energy infrastructure. However, in the medium term, sustained elevation of price requires structural supply loss or prolonged disruption of transit routes. Importantly, OPEC+ has already signaled supply flexibility in response to heightened geopolitical risk and a small increase in oil production. Their response function matters. Structurally higher energy prices could cause demand destruction, policy retaliation from consuming nations, and accelerated energy transition pressures. Energy prices can spike on short-term delivery and power generation worries, but sustained elevation requires structural supply loss.

Last summer, I sat on a panel talking about commodities as a part of an investment portfolio and argued that oil remains one of the most effective geopolitical hedges in a diversified portfolio. The rationale was that to hedge against geopolitical risk, oil and energy commodities are often cleaner than equity volatility products, particularly when the crude curve is backwardated and offers positive roll yield. In a multipolar world where conflict frequency may rise, even if magnitude does not, energy markets respond immediately to geopolitical stress. Commodities provide that structural diversification against fragmentation risk. It is also important for investors to have a breadth of commodity exposure within their portfolio, as today’s example is a great illustration of why having exposure to commodities like global LNG and coal can help to increase the robustness of energy-related geopolitical hedges.

Within the Viewpoint Diversified Commodities strategy, our energy exposure is sized within a risk-parity framework to participate in geopolitical risk premia without relying on a single headline outcome. Importantly, our energy exposure is diversified outside of just exposure to crude and U.S. natural gas, including global LNG benchmarks like Dutch and UK natural gas, along with exposure to Rotterdam coal.

For Viewpoint Enhanced Global Multi-Asset, the quantitative long/short commodity overlay has been adaptive to changing price trends throughout the year and was in a good position to take advantage of the heightened volatility in energy markets. Throughout the second half of 2025, the strategy was underweight WTI and Brent crude oil, as well as global LNG as geopolitical risk premia compressed. That dynamic flipped in early 2026. Exposure was rebuilt, and the strategy moved net long near the end of January, positioning to benefit as the risk premium rebuilt. This systematic shift, from defensive reduction to constructive re-engagement, reflects the adaptive nature of the strategy. It is designed not to forecast headlines, but to respond to evolving price structure, momentum, and cross-commodity dispersion.

While I expect tensions are likely to eventually de-escalate through negotiation, the near-term environment favours episodic volatility and geopolitical risk premia in both oil, LNG, and power generation markets. U.S. midterm gravity still exists and affordability for consumers still matters, therefore, U.S. domestic political tolerance for sustained energy price spikes remains limited. But in the short term, energy markets are behaving exactly as geopolitical hedges should. In a multipolar world, portfolios that lack sufficient commodity exposure may be structurally under-hedged, not just against oil shocks, but against broader energy-system disruption.

Happy investing!

Scott Smith

Chief Investment Officer

ABOUT THE AUTHOR

DISCLAIMER:

This blog and its contents are for informational purposes only. Information relating to investment approaches or individual investments should not be construed as advice or endorsement. Any views expressed in this blog were prepared based upon the information available at the time and are subject to change. All information is subject to possible correction. In no event shall Viewpoint Investment Partners Corporation be liable for any damages arising out of, or in any way connected with, the use or inability to use this blog appropriately.